—

0:00

FCA Regulatory Initiatives Grid December 2025: Complete UK Financial Regulation Guide

Table of Contents

- Understanding the FCA Regulatory Initiatives Grid Structure

- Consumer Duty: The Ongoing Regulatory Transformation

- Payments, Open Banking, and the National Payments Vision

- Crypto, Digital Assets, and FCA Regulatory Oversight

- ESG, Sustainable Finance, and Climate Disclosure Requirements

- Basel 3.1 Implementation and Prudential Reforms

- SM&CR Reform: Reducing Regulatory Burden

- Operational Resilience and Third-Party Risk Management

- Key Regulatory Milestones and Timeline for Financial Firms

- Strategic Implications for UK Financial Services Firms

🔑 Key Takeaways

- Understanding the FCA Regulatory Initiatives Grid Structure — The FCA Regulatory Initiatives Grid is organized into eight major sector categories, each covering distinct areas of financial services regulation.

- Consumer Duty: The Ongoing Regulatory Transformation — The Consumer Duty remains one of the most significant regulatory developments in UK financial services, and the December 2025 Grid reveals extensive follow-up activity that will continue to shape industry practices through 2026 and beyond.

- Payments, Open Banking, and the National Payments Vision — The payments sector features prominently in the FCA Regulatory Initiatives Grid, reflecting the transformative changes underway in UK payment infrastructure and digital finance.

- Crypto, Digital Assets, and FCA Regulatory Oversight — The regulatory treatment of cryptoassets and digital assets continues to evolve rapidly, and the December 2025 Grid provides important signals about the UK’s approach to this emerging sector.

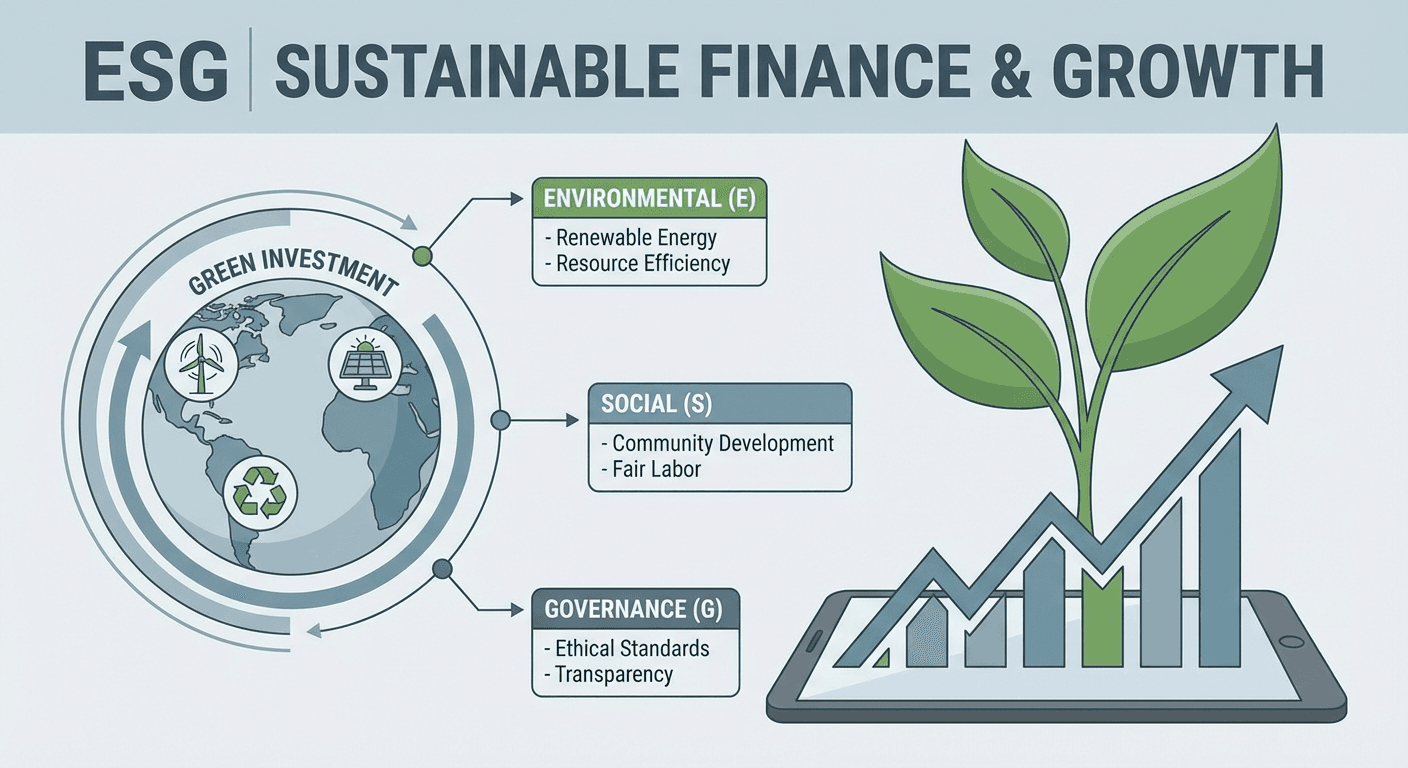

- ESG, Sustainable Finance, and Climate Disclosure Requirements — Environmental, Social, and Governance (ESG) regulation is among the most dynamic areas in the FCA Regulatory Grid, with multiple interconnected initiatives that will reshape how financial services firms approach sustainability.

Understanding the FCA Regulatory Initiatives Grid Structure

The FCA Regulatory Initiatives Grid is organized into eight major sector categories, each covering distinct areas of financial services regulation. This structure allows firms to quickly identify the initiatives most relevant to their operations and plan their compliance resources accordingly.

The Grid’s main sectors include: Multi-sector initiatives (the largest category, covering cross-cutting regulatory changes), Banking, credit and lending, Payments and cryptoassets, Insurance and reinsurance, Investment management, Pensions and retirement income, Retail investments, and Wholesale financial markets. Each initiative is classified by its lead regulatory body, current status, expected timeline, and anticipated impact on firms.

The Forum’s nine member organizations comprise the Bank of England, Competition and Markets Authority (CMA), Financial Conduct Authority (FCA), Financial Reporting Council (FRC), His Majesty’s Treasury (HMT), Information Commissioner’s Office (ICO), Prudential Regulation Authority (PRA), Payment Systems Regulator (PSR), and The Pensions Regulator (TPR). This breadth of membership ensures comprehensive coverage of the UK regulatory landscape. For perspective on how central banks approach financial regulation, explore our ECB Annual Report 2024 interactive analysis.

Consumer Duty: The Ongoing Regulatory Transformation

The Consumer Duty remains one of the most significant regulatory developments in UK financial services, and the December 2025 Grid reveals extensive follow-up activity that will continue to shape industry practices through 2026 and beyond.

Key Consumer Duty developments in the Grid include:

- Supervisory approach statement: Published December 8, 2025, clarifying how the FCA will supervise firms’ compliance with Consumer Duty obligations

- Targeted Handbook clarifications: Published December 9, 2025, addressing specific areas where firms have sought guidance

- Scope and distribution chain consultation: Planned for H1 2026, this consultation will address the application of Consumer Duty across complex distribution chains

- Call for Input follow-ups: The FCA’s review of requirements following Consumer Duty introduction continues, with further consultations planned for mid-2026

The Consumer Duty has fundamentally changed the regulatory compact between firms and customers in the UK. Rather than prescriptive rules about specific products or practices, the Duty requires firms to deliver good outcomes for retail customers across four key areas: products and services, price and value, consumer understanding, and consumer support. The ongoing work reflected in the Grid shows that the FCA views Consumer Duty not as a one-time implementation exercise but as an evolving framework that will continue to be refined and expanded.

Explore Interactive Experience →

Payments, Open Banking, and the National Payments Vision

The payments sector features prominently in the FCA Regulatory Initiatives Grid, reflecting the transformative changes underway in UK payment infrastructure and digital finance. The National Payments Vision (NPV) serves as the strategic framework driving multiple interconnected initiatives.

Smart Data and Open Banking: Treasury’s Data (Use and Access) Act provides the legal foundation for Smart Data schemes, with the Open Banking statutory instrument expected Q4 2026. The FCA has committed to publishing a road map for Open Finance before March 2026, signaling the expansion of open data principles beyond banking into insurance, pensions, and investment products.

Variable Recurring Payments (VRP): The PSR is delivering Phase 1 of VRP, with market go-live in H2 2025. VRP represents a fundamental evolution in how consumers and businesses manage recurring payments, offering greater control and flexibility compared to traditional direct debits.

Regulatory Responsibility Transfer: The FCA is assuming greater responsibility for Open Banking oversight, taking forward outstanding JROC (Joint Regulatory Oversight Committee) actions. This transition reflects the maturation of Open Banking from an innovative concept to a core part of the UK’s financial infrastructure that requires ongoing regulatory stewardship.

These payments initiatives collectively represent one of the most ambitious regulatory reform programs in the Grid, with the potential to fundamentally reshape how money moves through the UK economy. For firms operating in the payments space, the timeline of changes requires careful planning and significant technology investment. Understanding these shifts is critical, as explored in our Federal Reserve Financial Stability Report 2025 for parallel regulatory developments in the US financial system.

📊 Explore this analysis with interactive data visualizations

Crypto, Digital Assets, and FCA Regulatory Oversight

The regulatory treatment of cryptoassets and digital assets continues to evolve rapidly, and the December 2025 Grid provides important signals about the UK’s approach to this emerging sector.

PRA Crypto Prudential Framework: The PRA is developing rules to implement the Basel standard for the prudential treatment of firms’ exposures to cryptoassets. A Consultation Paper is expected Q4 2026, which will establish capital requirements and risk management standards for banks and financial institutions holding or trading crypto assets. The indicative impact on firms is classified as low, suggesting a proportionate approach.

ICO Guidance on Distributed Ledger Technologies (DLT): The Information Commissioner’s Office launched a public consultation in August 2025 on draft guidance covering privacy and data protection issues arising from DLT deployments. This guidance addresses the inherent tension between blockchain’s immutable record-keeping and data protection requirements including the right to erasure.

Stablecoin Regulation: The Grid references ongoing initiatives related to stablecoins, positioning the UK as a jurisdiction that seeks to support innovation while establishing appropriate consumer protections and financial stability safeguards. The regulatory approach aims to bring stablecoin issuers and service providers within the FCA’s perimeter.

For deeper analysis of the crypto regulatory landscape, our State of Crypto 2025 from a16z provides comprehensive market context, while our Cryptocurrency Guide offers foundational understanding of digital asset markets.

ESG, Sustainable Finance, and Climate Disclosure Requirements

Environmental, Social, and Governance (ESG) regulation is among the most dynamic areas in the FCA Regulatory Grid, with multiple interconnected initiatives that will reshape how financial services firms approach sustainability.

ESG Ratings Regulation: In a landmark move, HMT laid draft legislation on October 27, 2025, to bring ESG ratings providers within the FCA’s regulatory perimeter. The FCA opened its consultation on December 1, 2025, with responses due by March 31, 2026. This initiative addresses concerns about the transparency, methodology, and potential conflicts of interest in the ESG ratings industry — a sector that has grown enormously influential in directing capital allocation decisions.

UK Sustainability Reporting Standards (UK SRS): Building on the UK’s endorsement of ISSB standards, the Department for Business and Trade (DBT) consulted on company disclosure requirements through September 2025. The FCA intends to consult in January 2026 on disclosure requirements for UK listed companies, creating a comprehensive sustainability reporting framework aligned with international standards.

Sustainability Disclosure Requirements (SDR): The FCA’s SDR rules, including investment product labeling requirements, are in force. However, the portfolio manager rules have been paused, indicating the regulator’s willingness to adjust implementation timelines based on market readiness and practical considerations.

FRC Stewardship Code 2026: The revised Stewardship Code takes effect January 1, 2026, setting new expectations for how asset owners and managers integrate stewardship and sustainability considerations into their investment processes. For a broader view of global economic sustainability factors, see our IMF World Economic Outlook October 2024 analysis.

Basel 3.1 Implementation and Prudential Reforms

The continued implementation of Basel 3.1 standards remains a cornerstone of the UK’s prudential regulatory framework, and the Grid confirms that this multi-year program continues to advance alongside the complementary Strong and Simple framework designed for smaller banks and building societies.

Key prudential initiatives in the Grid include:

| Initiative | Lead Body | Timeline | Impact |

|---|---|---|---|

| Basel 3.1 Standards Implementation | PRA | Ongoing through 2027 | High |

| Strong and Simple Framework | PRA | Phased implementation | Medium |

| Crypto Prudential Treatment (Basel) | PRA | CP Q4 2026 | Low |

| Market Risk Capital (Specialised Trading) | FCA | EP Dec 2025, CP H2 2026 | Medium |

| Prospectus Regime Reform | FCA/HMT | Ongoing | Medium |

The Basel 3.1 implementation is particularly significant for UK banks as it standardizes how capital requirements are calculated across credit risk, market risk, operational risk, and output floor provisions. The PRA’s approach balances international consistency with UK-specific considerations, reflecting the post-Brexit freedom to tailor prudential standards to the UK’s financial sector structure.

The Strong and Simple framework represents an important innovation in prudential regulation, recognizing that smaller, domestically-focused financial institutions require proportionate regulatory treatment that reflects their lower systemic risk profile. This framework aims to reduce compliance costs for qualifying firms while maintaining appropriate safety standards.

📊 Explore this analysis with interactive data visualizations

SM&CR Reform: Reducing Regulatory Burden

The Senior Managers and Certification Regime (SM&CR) is undergoing significant reform, with the Grid confirming that HMT and regulators are targeting approximately 50% reduction in the regime’s burden on firms. Consultations closed in October 2025, with first-phase implementation expected around mid-2026.

The SM&CR reforms respond to widespread industry feedback that the original regime, while well-intentioned in promoting individual accountability, has created disproportionate compliance costs, particularly for smaller firms. The reforms aim to streamline certification processes, reduce prescriptive requirements, and focus the regime more tightly on senior individuals who genuinely have the power to influence firm behavior.

For firms, these reforms represent a welcome opportunity to redirect compliance resources toward areas of greater risk and value. However, the phased implementation approach means that firms will need to manage the transition carefully, maintaining compliance with current requirements while preparing for the reformed regime. Primary legislation is expected for further-reaching reforms beyond what can be achieved through regulatory rules alone, according to the official FCA Grid document.

Operational Resilience and Third-Party Risk Management

Operational resilience continues to climb the regulatory agenda, with the Grid highlighting several coordinated initiatives between the BoE, FCA, and PRA that will establish comprehensive requirements for incident reporting, outsourcing oversight, and third-party risk management.

Incident, Outsourcing and Third-Party Reporting: Following the coordinated consultation published in December 2024, final rules and a Policy Statement are expected in H1 2026, with implementation required 12 months later (effectively H1 2027). This initiative creates a unified framework for reporting significant operational incidents and managing risks from outsourcing arrangements and critical third-party providers.

Transforming Data Collections: This multi-strand programme aims to streamline and modernize how regulators collect data from firms. A Quarterly Consultation Paper published December 5, 2025, addresses the decommissioning of some reporting returns, with further Handbook notices expected in H1 2026. The programme promises to reduce reporting burden while improving data quality and regulatory effectiveness.

These initiatives reflect the growing recognition that financial stability depends not just on capital adequacy and conduct standards, but on the operational resilience of the technology infrastructure that underpins modern financial services. The increasing reliance on cloud computing, AI systems, and interconnected digital platforms makes operational resilience a first-order regulatory concern.

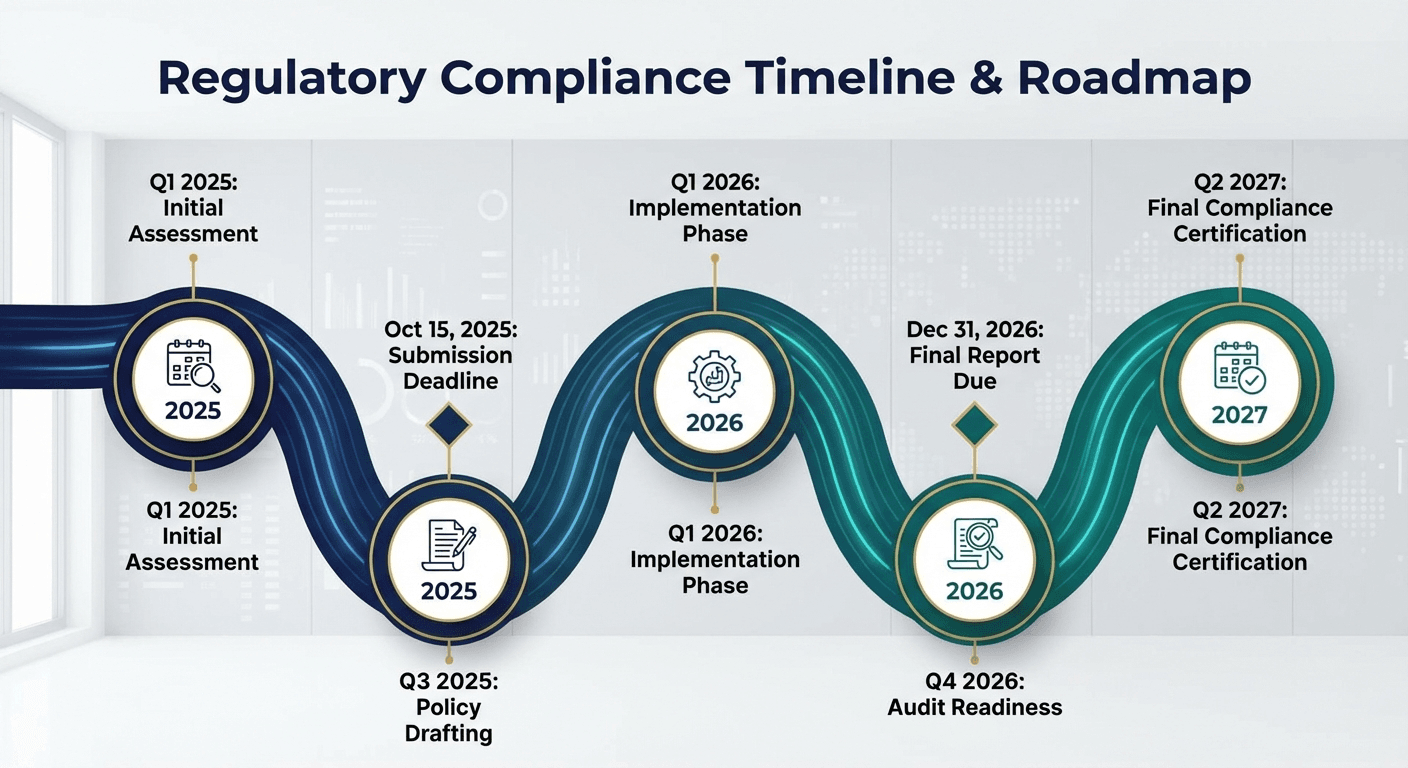

Key Regulatory Milestones and Timeline for Financial Firms

For compliance teams and strategic planners, the Grid’s timeline of upcoming milestones is essential for resource allocation and project planning. Here are the critical dates that financial services firms should have on their radar:

| Timeline | Initiative | Action Required |

|---|---|---|

| Jan 1, 2026 | BFSA Takes Effect / FRC Stewardship Code 2026 | Compliance required for affected firms |

| Jan-Mar 2026 | Advice Guidance Boundary Review SI | Prepare for new “targeted support” activity |

| Mar 31, 2026 | ESG Ratings Consultation Closes | Submit responses to FCA CP |

| Apr-Jun 2026 | Advice Guidance Boundary Regime Goes Live | Implement new advice/guidance framework |

| Mid-2026 | SM&CR First-Phase Implementation | Adapt to reformed accountability regime |

| H1 2026 | Incident/Outsourcing Final Rules Published | Begin 12-month implementation period |

| Q4 2026 | Open Banking SI / PRA Crypto CP | Prepare for Smart Data requirements |

| H1 2027 | Incident/Outsourcing Implementation Due | Full compliance required |

| Jul 2027 | New Complaints Reporting Go-Live | Implement consolidated reporting system |

Strategic Implications for UK Financial Services Firms

The FCA Regulatory Initiatives Grid December 2025 carries several strategic implications that firms should consider when planning their regulatory change programmes and business strategies.

Regulatory consolidation is underway: The 13% reduction in live initiatives signals that regulators are conscious of the cumulative burden of regulatory change and are actively working to streamline their pipelines. The high proportion of joint initiatives (45 out of 124) suggests improved coordination between regulatory bodies.

The growth agenda is genuine: Multiple initiatives are explicitly linked to the Government’s growth agenda and the Financial Services Growth and Competitiveness Strategy. This creates a more favorable environment for innovation and market development than firms may have experienced in previous regulatory cycles.

Technology investment is non-negotiable: Initiatives around data collection transformation, operational resilience, Open Banking, and digital assets all require significant technology investment. Firms that underinvest in their technology capabilities will find it increasingly difficult to comply with regulatory requirements efficiently.

International alignment matters: The Grid reflects the UK’s ongoing effort to maintain international regulatory alignment (through Basel 3.1, ISSB endorsement, and Berne Financial Services Agreement) while exercising post-Brexit regulatory sovereignty. Firms operating across multiple jurisdictions need to monitor both UK-specific and international regulatory developments.

For the latest analysis of global financial stability considerations that intersect with UK regulatory developments, the Bank of England’s Financial Stability page and the FCA’s official Regulatory Grid portal provide essential reference material.

📊 Explore this analysis with interactive data visualizations