NVIDIA 10-K FY2025 Analysis: $130.5 Billion Revenue, AI Dominance, and What Investors Need to Know

Table of Contents

- Executive Summary: NVIDIA's Record-Breaking FY2025

- Revenue Breakdown: Where the $130.5 Billion Came From

- Data Center Dominance: The $115 Billion AI Engine

- Profitability and Margins: Reading Between the Numbers

- Blackwell Architecture: NVIDIA's Next Frontier

- Competitive Landscape: AMD, Intel, and Custom Silicon

- Risk Factors: What Could Slow the AI Juggernaut

- Balance Sheet Strength and Capital Allocation

- Forward Outlook and What FY2026 Could Bring

- Investor Takeaways from the NVIDIA 10-K Filing

📌 Key Takeaways

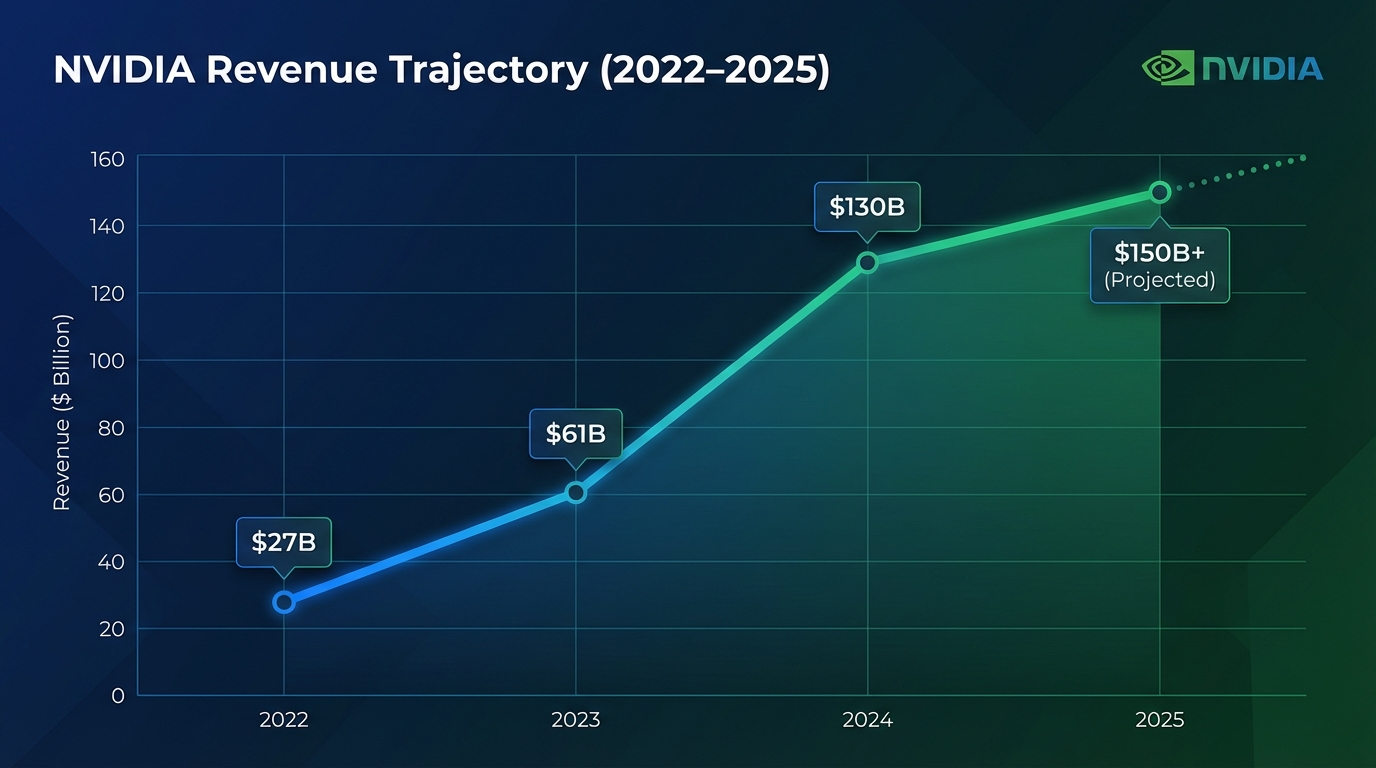

- $130.5B in Revenue: NVIDIA more than doubled its top line, growing 114% year-over-year in FY2025 — an unprecedented feat for a company of its scale.

- Data Center = 88% of Revenue: The Data Center segment hit $115.2B (up 142%), cementing NVIDIA as the backbone of global AI infrastructure.

- $72.9B Net Income: GAAP net income surged 145%, with non-GAAP earnings per share reaching $2.99 — making NVIDIA one of the most profitable companies in history.

- Blackwell Launched: The next-gen architecture achieved billions in first-quarter sales, signaling sustained demand despite margin pressure.

- $60.7B Free Cash Flow: Massive cash generation enabled $33.7B in share buybacks while maintaining $43.2B in cash reserves.

Executive Summary: NVIDIA's Record-Breaking FY2025

NVIDIA Corporation's Form 10-K for fiscal year 2025 (ended January 26, 2025) tells the story of a company that has become synonymous with the AI revolution. With full-year revenue of $130.5 billion — up 114% from the prior year — NVIDIA delivered one of the most extraordinary growth periods in corporate history.

The numbers are staggering by any measure. Revenue more than doubled. Net income reached $72.9 billion, up 145%. Operating income hit $81.5 billion. And the company generated $60.7 billion in free cash flow — enough to fund an entire national space program. This NVIDIA annual report 10-K analysis breaks down what drove these results, where risks lie, and what the filing reveals about the company's strategic direction.

For investors, analysts, and technology professionals trying to understand the AI infrastructure buildout — and with NVIDIA now powering over 75% of the world's TOP500 supercomputers — this NVIDIA 10-K analysis provides a comprehensive look at the financial engine powering the world's AI ambitions. The filing reveals not just where NVIDIA has been, but where it is headed — from the broader AI landscape documented in the Stanford AI Index 2025 to the specific infrastructure that makes it all possible.

Revenue Breakdown: Where the $130.5 Billion Came From

Understanding NVIDIA's FY2025 financial results requires examining how its revenue is distributed across business segments. The company operates through two reportable segments — Compute & Networking and Graphics — but the market-facing revenue breakdown reveals four key areas:

| Segment | FY2025 Revenue | FY2024 Revenue | Y/Y Growth |

|---|---|---|---|

| Data Center | $115.2B | $47.5B | +142% |

| Gaming | $11.4B | $10.4B | +9% |

| Professional Visualization | $1.9B | $1.6B | +21% |

| Automotive & Robotics | $1.7B | $1.1B | +55% |

The concentration is immediately apparent: Data Center revenue represents approximately 88% of NVIDIA's total business, up from 78% in the prior year. This is both NVIDIA's greatest strength and, as the 10-K risk factors acknowledge, a source of concentration risk. The gaming segment, once NVIDIA's bread and butter, now accounts for less than 9% of revenue despite generating $11.4 billion — a number that would be the envy of most technology companies.

The Automotive and Robotics segment, while the smallest at $1.7 billion, showed the second-fastest growth rate at 55%. NVIDIA's DRIVE platform partnerships with Toyota, Hyundai, and other automakers position this segment as a potentially significant long-term revenue driver as autonomous vehicles and robotics adoption accelerates.

Data Center Dominance: The $115 Billion AI Engine

NVIDIA's Data Center revenue of $115.2 billion in FY2025 is the headline number that defines this 10-K filing. The 142% year-over-year growth was driven by what the company describes as "demand for our Hopper architecture accelerated computing platform used for large language models, recommendation engines, and generative AI applications."

To put this in perspective: NVIDIA's data center revenue alone is larger than the total revenue of companies like Intel ($54.2B in 2024), AMD ($25.8B), or Qualcomm ($38.9B). The company has effectively built a monopoly-like position in AI training and inference hardware, with major cloud service providers — AWS, Microsoft Azure, Google Cloud, and Oracle Cloud — all deploying NVIDIA's infrastructure at massive scale.

Fourth quarter data center revenue was $35.6 billion, up 93% year-over-year and 16% sequentially. The Q4 acceleration indicates that demand is not only sustained but accelerating, driven by the initial ramp of the Blackwell architecture. The 10-K notes that NVIDIA is a "key technology partner" for the $500 billion Stargate Project, an AI infrastructure initiative that underscores the scale of investment flowing into AI compute.

"Demand for Blackwell is amazing as reasoning AI adds another scaling law — increasing compute for training makes models smarter and increasing compute for long thinking makes the answer smarter." — Jensen Huang, CEO, NVIDIA

This growth trajectory has significant implications for the broader financial markets, as outlined in JP Morgan's 2025 Market Outlook. NVIDIA's capital expenditure requirements from cloud providers alone represent a meaningful share of global technology investment.

Explore NVIDIA's complete 10-K filing as an interactive experience — easier to navigate than a 100+ page SEC document.

Profitability and Margins: Reading Between the Numbers

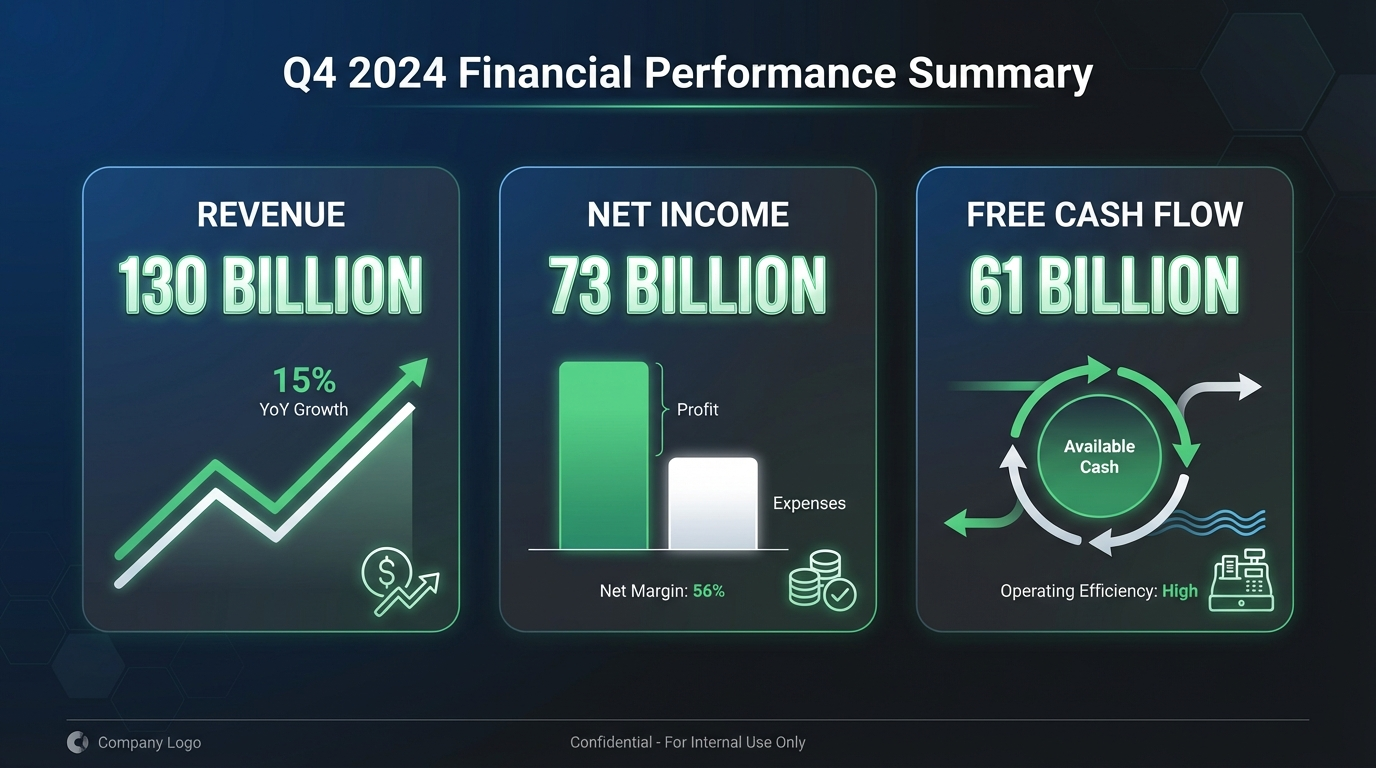

NVIDIA's FY2025 profitability metrics are exceptional by any standard. GAAP gross margin came in at 75.0%, up from 72.7% in FY2024 — an improvement that reflects the pricing power NVIDIA commands in a supply-constrained market. Non-GAAP gross margin was 75.5%, up 1.7 percentage points year-over-year.

Key Profitability Metrics

| Metric | FY2025 | FY2024 | Change |

|---|---|---|---|

| Revenue | $130.5B | $60.9B | +114% |

| Gross Profit (GAAP) | $97.9B | $44.3B | +121% |

| Gross Margin (GAAP) | 75.0% | 72.7% | +2.3 pts |

| Operating Income (GAAP) | $81.5B | $33.0B | +147% |

| Net Income (GAAP) | $72.9B | $29.8B | +145% |

| EPS (Diluted, GAAP) | $2.94 | $1.19 | +147% |

| Free Cash Flow | $60.7B | $26.9B | +126% |

However, there is a notable trend within the year that investors should watch carefully. Q4 FY2025 GAAP gross margin was 73.0%, down from 76.0% in Q4 FY2024 — a 3.0 percentage point decline. This reflects the initial costs associated with ramping Blackwell production. NVIDIA's Q1 FY2026 guidance projects gross margins of approximately 70.6% (GAAP), suggesting further near-term compression as the new architecture scales.

Operating expenses grew 45% to $16.4 billion, with research and development spending reaching $12.9 billion (up 49%). This R&D investment — nearly 10% of revenue — reflects NVIDIA's commitment to maintaining its technological lead. By comparison, operating expenses grew far slower than revenue, demonstrating significant operating leverage in the business model.

Blackwell Architecture: NVIDIA's Next Frontier

The most forward-looking element of the NVIDIA 10-K FY2025 filing is the launch and initial ramp of the Blackwell architecture. Unlike previous GPU generations, Blackwell represents "a full set of data center scale infrastructure that includes GPUs, CPUs, DPUs, interconnects, switch chips and systems, and networking adapters."

This systems-level approach is strategically significant. NVIDIA is no longer selling individual chips — it is selling complete AI infrastructure solutions. The GB200 systems are being deployed by AWS, CoreWeave, Google Cloud, Microsoft Azure, and Oracle Cloud, indicating broad adoption across the hyperscaler ecosystem.

Key Blackwell developments from the 10-K include:

- Billions in first-quarter sales — achieving rapid revenue ramp despite the complexity of a new architecture

- Excels at generative AI — optimized specifically for the AI workloads driving current demand

- Data center-scale design — not just GPUs, but complete infrastructure including networking (Spectrum-X)

- Near-term margin impact — production costs are temporarily compressing gross margins to ~71%

The Blackwell architecture also extends to the consumer market through the GeForce RTX 50 Series, featuring DLSS 4 with Multi Frame Generation. This technology leverages AI to generate additional frames, delivering up to 2x performance improvement over the prior generation. For those interested in the underlying AI technology, the Transformer architecture that powers these capabilities is well-documented.

Competitive Landscape: AMD, Intel, and Custom Silicon

While NVIDIA's dominance is clear from the financial results, the 10-K filing also reveals a competitive landscape that is evolving rapidly. Understanding where NVIDIA stands relative to competitors is essential for any comprehensive NVIDIA 10-K analysis.

AMD: The Closest Challenger

AMD's MI300 series accelerators have gained traction, with the company reporting $5.0 billion in data center GPU revenue in calendar year 2024. While this represents meaningful progress, it is still a fraction of NVIDIA's $115.2 billion data center business. AMD's roadmap includes the MI350 and MI400 architectures, which aim to narrow the performance gap — but NVIDIA's software ecosystem (CUDA) remains a significant competitive moat.

Intel: Restructuring and Catching Up

Intel's Gaudi accelerators have struggled to gain meaningful market share in AI training. The company's broader restructuring and the separation of its foundry business have diverted attention and resources from the AI accelerator market. Intel remains a factor in CPU-based inference but is not currently a direct competitor to NVIDIA's GPU dominance.

Custom Silicon: The Long-Term Threat

Perhaps the most significant competitive dynamic discussed in NVIDIA's risk factors is the trend toward custom AI accelerators built by its largest customers. Google's TPUs, Amazon's Trainium/Inferentia chips, Microsoft's Maia, and Meta's MTIA represent a growing effort by hyperscalers to reduce dependence on NVIDIA. While these custom solutions currently complement rather than replace NVIDIA's GPUs, they represent a long-term structural risk to market share.

Turn dense financial filings into clear, interactive experiences your team will actually read.

Risk Factors: What Could Slow the AI Juggernaut

NVIDIA's 10-K filing devotes considerable attention to risk factors, and prudent investors should pay close attention. Despite the extraordinary financial performance, several risks could materially impact future results:

1. Customer Concentration

The filing reveals that a small number of customers — primarily large cloud service providers — account for a disproportionate share of revenue. In FY2025, customers representing 10% or more of total revenue were primarily in the Compute & Networking segment. This concentration means that a single customer's decision to reduce orders or shift to alternative solutions could meaningfully impact NVIDIA's results.

2. Export Restrictions and Geopolitical Risk

U.S. government restrictions on exports of advanced AI chips to China and other countries continue to evolve and could expand. NVIDIA has already been forced to create China-specific products with reduced capabilities. The 10-K acknowledges that further restrictions could reduce revenue and accelerate the development of competitive alternatives by Chinese semiconductor companies.

3. Supply Chain Dependencies

NVIDIA relies on Taiwan Semiconductor Manufacturing Company (TSMC) for virtually all of its advanced chip manufacturing. Any disruption to TSMC's operations — whether from geopolitical tensions, natural disasters, or capacity constraints — would directly impact NVIDIA's ability to meet demand. This risk is amplified by the current supply-constrained environment.

4. Margin Compression Risk

As the Blackwell architecture ramps, gross margins are under pressure. NVIDIA's Q1 FY2026 guidance of ~70.6% GAAP gross margin represents a meaningful decline from the 75.0% achieved in FY2025. If this compression deepens or persists beyond the initial ramp period, it could signal structural changes in NVIDIA's pricing power.

5. Regulatory Environment

The global regulatory landscape for AI is evolving rapidly. The EU AI Act and similar regulations in other jurisdictions could impact how NVIDIA's technology is deployed and sold. While the direct impact on hardware sales may be limited, regulatory requirements on NVIDIA's customers could indirectly affect demand patterns.

Balance Sheet Strength and Capital Allocation

NVIDIA ended FY2025 with a fortress balance sheet. Total assets reached $111.6 billion, up from $65.7 billion in the prior year. The company's financial position provides enormous strategic flexibility:

- Cash and marketable securities: $43.2 billion (up from $26.0B)

- Total debt: $8.5 billion in long-term debt (unchanged from prior year)

- Net cash position: Approximately $34.7 billion

- Shareholders' equity: $79.3 billion (up from $43.0B)

Capital allocation in FY2025 was aggressive. NVIDIA repurchased $33.7 billion of its own shares — a massive return of capital to shareholders. The company also invested $3.2 billion in property and equipment and $1.5 billion in non-marketable equity securities. Total operating cash flow of $64.1 billion gave NVIDIA ample room to fund these activities while still growing its cash reserves.

The 10-K also reveals that NVIDIA paid $15.1 billion in cash income taxes during FY2025, making it one of the largest corporate taxpayers globally. This detail is relevant for investors assessing the company's effective tax rate and potential impacts from changes in international tax policy.

For context on how NVIDIA's financial metrics compare within the broader market environment, the Federal Reserve's Financial Stability Report provides useful background on the macroeconomic conditions supporting technology investment.

Forward Outlook and What FY2026 Could Bring

NVIDIA's Q1 FY2026 guidance of approximately $43 billion in revenue represents a 78% year-over-year increase from Q1 FY2025 ($22.1B). If this growth rate is sustained, FY2026 could see revenue approaching $180-200 billion — a figure that would have seemed inconceivable just two years ago.

Several catalysts support continued growth:

Agentic AI and Reasoning Models

Jensen Huang explicitly identified "reasoning AI" as adding "another scaling law" to compute demand. As AI models shift from simple inference to complex reasoning and agentic behaviors — where models take autonomous actions — the compute requirements multiply. Each "thinking" step requires additional GPU cycles, expanding the total addressable market for NVIDIA's hardware.

Physical AI and Robotics

NVIDIA's Cosmos platform for world foundation models, the Jetson edge computing platform, and the DRIVE autonomous vehicle platform position the company for the next wave of AI applications in the physical world. The partnership with Toyota and Hyundai signals automotive industry adoption at scale.

Sovereign AI Infrastructure

Governments worldwide are investing in national AI computing infrastructure. NVIDIA's partnerships with sovereign entities and the opening of R&D centers (including a new facility in Vietnam) reflect this trend. These government-funded projects typically involve large, multi-year commitments.

Enterprise AI Adoption

Beyond hyperscalers, enterprises are increasingly deploying AI infrastructure. Cisco's integration of NVIDIA Spectrum-X into its networking portfolio, Verizon's edge AI partnership, and healthcare collaborations with IQVIA and Mayo Clinic illustrate broadening enterprise adoption. According to PwC's Global CEO Survey 2025, AI adoption is a top priority for enterprise leaders worldwide.

Stay ahead of market shifts — transform financial reports into interactive experiences for your investment research.

Investor Takeaways from the NVIDIA 10-K Filing

NVIDIA's FY2025 10-K filing paints a picture of a company at the apex of the AI revolution. The financial performance is extraordinary — $130.5 billion in revenue, $72.9 billion in net income, $60.7 billion in free cash flow — but the filing also reveals the challenges and risks that come with this position.

For long-term investors, several key themes emerge from this NVIDIA 10-K analysis:

- The AI infrastructure buildout is still early. Despite NVIDIA's massive growth, demand continues to outpace supply. The company's guidance suggests accelerating, not decelerating, revenue growth in FY2026.

- Margin compression is real but likely temporary. The Blackwell ramp is pressuring gross margins, but historical precedent suggests margins will recover as production scales and costs are optimized.

- Customer concentration is a structural risk. NVIDIA's dependence on a handful of hyperscale cloud providers creates vulnerability. Diversification into automotive, robotics, and enterprise markets is strategically important.

- The software moat deepens. CUDA's ecosystem lock-in, combined with NVIDIA AI Enterprise, NIM microservices, and Omniverse, creates switching costs that go far beyond hardware specifications.

- Geopolitical risk is the wild card. Export restrictions, TSMC dependence, and evolving AI regulations could materially impact NVIDIA's trajectory in ways that financial models struggle to capture.

NVIDIA's 10-K filing is essential reading for anyone with exposure to AI, semiconductors, or the broader technology sector. The company's financial performance in FY2025 was historic, and its strategic positioning suggests the story is far from over. As documented in McKinsey's State of AI 2025 report, the enterprise AI adoption cycle is still in its early innings — and NVIDIA stands to be its primary beneficiary.

Frequently Asked Questions

What was NVIDIA's total revenue in fiscal year 2025?

NVIDIA reported record full-year revenue of $130.5 billion for fiscal year 2025 (ended January 26, 2025), representing a 114% increase from $60.9 billion in the prior fiscal year. The growth was primarily driven by explosive demand for AI accelerators in data center environments.

How much did NVIDIA's data center segment grow in FY2025?

NVIDIA's Data Center segment generated $115.2 billion in revenue during FY2025, an increase of 142% year-over-year. This segment alone accounted for approximately 88% of total company revenue, driven by demand for Hopper and Blackwell architecture GPUs used in AI training and inference workloads.

What is NVIDIA's Blackwell architecture and why does it matter?

Blackwell is NVIDIA's newest GPU architecture launched during FY2025. It represents a full data center-scale infrastructure including GPUs, CPUs, DPUs, interconnects, switch chips, systems, and networking adapters. Blackwell achieved billions of dollars in sales in its first quarter and is designed to excel at generative AI and accelerated computing workloads.

What are the main risk factors in NVIDIA's 10-K filing?

Key risk factors include: customer concentration (major cloud providers represent significant revenue), US and international export restrictions on AI chips (particularly to China), supply chain constraints for advanced semiconductors, intense competition from AMD and custom silicon from cloud providers, potential margin compression from Blackwell production ramp-up costs, and regulatory risks around AI technology globally.

What is NVIDIA's outlook for fiscal year 2026?

NVIDIA guided Q1 FY2026 revenue at approximately $43 billion (plus or minus 2%), suggesting continued strong growth. However, gross margins are expected to dip to approximately 71% as Blackwell production scales. CEO Jensen Huang highlighted surging demand from agentic AI and physical AI as the next growth drivers.