Venture Capital Trends Q3 2025: The Complete PitchBook NVCA Venture Monitor Analysis

Table of Contents

- US Venture Capital Market Overview Q3 2025

- Venture Capital Dealmaking: Record Value Despite Fewer Deals

- AI and Machine Learning Dominate VC Investment

- IPO Market Recovery: Tech vs. Biotech Divergence

- Megadeals and Unicorn Valuations Surge

- VC Fundraising Hits Multi-Year Lows

- Exit Environment and M&A Acceleration

- Female Founders and Diversity in Venture Capital

- Regional Venture Capital Spotlight

- NVCA Policy Highlights and Regulatory Shifts

📌 Key Takeaways

- $250.2B deployed through Q3 2025 — already surpassing full-year totals for 2022–2024, driven by concentrated AI megadeals

- AI captures 64.3% of deal value — with only 37.5% of deal count, signaling extreme capital concentration in artificial intelligence

- Nine billion-dollar-plus rounds in Q3 — accounting for nearly 40% of quarterly deal value, led by Anthropic ($13B), xAI ($10B), and Databricks ($1B)

- IPO recovery favors tech over biotech — tech IPOs represent 95.1% of value created through listings, while biotech saw only 8 IPOs versus 22 in 2024

- Fundraising at lowest since 2017 — with only $45.7B committed through Q3, as limited partners face a deepening liquidity crunch nearly four years after 2021 peaks

US Venture Capital Market Overview Q3 2025

The US venture capital ecosystem stands at a fascinating crossroads. According to the PitchBook NVCA Venture Monitor Q3 2025, total deal value through the first three quarters already reached $250.2 billion across an estimated 12,422 deals — surpassing the full-year totals for 2022, 2023, and 2024 combined. This venture capital trends report reveals a market defined by extraordinary concentration: a handful of elite AI-focused startups attracting the lion’s share of investment while thousands of other companies struggle to secure funding.

The bifurcation between the haves and have-nots has never been more pronounced. While mega-rounds grab headlines, the share of sub-$5 million deals fell to just 50.3% in 2025 — a decade low that illustrates how selective capital allocation has become. Founders increasingly opt for larger raises to extend their runways and defer future rounds, hoping market conditions will improve. Meanwhile, the liquidity crunch entering its fourth year since the 2021 peak has put unprecedented pressure on limited partners, with distributions still well below historical averages.

For investors, portfolio managers, and anyone tracking venture capital trends in 2025, this report provides the definitive data-driven assessment of where the market stands and where it’s heading. From AI’s dominance to the uneven IPO recovery, each section distills the critical insights from PitchBook’s comprehensive analysis into actionable intelligence.

Venture Capital Dealmaking: Record Value Despite Fewer Deals

Q3 2025 saw VC firms deploy $80.9 billion across approximately 4,208 deals, marking a 4.9% quarter-over-quarter increase in deal value. The full-year trajectory is remarkable: with $250.2 billion invested through September, 2025 is already the second-highest year on record for deal value, behind only 2021’s extraordinary $360 billion.

However, the headline numbers mask a deeper structural shift. Deal count has declined from the 2021 peak of 19,648 to an estimated 12,422 through Q3 2025, while the value has surged. This divergence is driven by the concentration of capital in larger rounds. The share of deals under $5 million — historically the backbone of early-stage venture — dropped to 50.3% from 57.0% in 2024, marking the lowest level in a decade.

Median deal sizes have increased across every stage. Series D+ median deal size reached $100 million, while even pre-seed rounds saw median values climb to $0.5 million. Series A median deal size hit $14 million, and Series B reached $32.4 million. These increases reflect both genuine growth in capital requirements (particularly for AI companies) and founders’ strategic decisions to raise larger rounds amid uncertain exit markets.

The dealmaking indicator remained firmly in investor-friendly territory throughout Q3, particularly at the late and venture-growth stages. This means investors continue to enjoy favorable terms, lower valuations relative to 2021, and stronger governance provisions — a dynamic that has persisted since the 2022 correction.

AI and Machine Learning Dominate VC Investment

Artificial intelligence has become the gravitational center of venture capital. In 2025 year-to-date, AI and machine learning companies accounted for a staggering 64.3% of all venture deal value — up from 50.2% in 2024 — while representing only 37.5% of deal count. This concentration is unprecedented in the history of venture capital, with AI deal value reaching $160.8 billion through Q3, already shattering the previous full-year record of $108.2 billion set in 2024.

The AI sector has seen median deal values soar to $6 million (up from $4.1 million in the prior year), while average deal values reached $58.9 million — reflecting the impact of billion-dollar-plus mega-rounds. Pre-money valuations tell a similar story: median AI & ML valuations reached $45 million, with average valuations hitting $1.06 billion, driven upward by the massive valuations of companies like Anthropic ($183 billion), xAI ($75 billion), and Databricks ($100 billion).

This level of investor conviction in AI comes with significant risks. As company valuations climb, the pressure to deliver outsized returns intensifies. The race to secure top talent, purchase chips, and build infrastructure requires extraordinary capital — but it also raises the bar for what these businesses must ultimately generate for their investors. History tells us that extreme market concentration carries inherent risks, and the AI boom echoes patterns seen in previous technology cycles. For a broader perspective on how AI is reshaping industries, explore our McKinsey State of AI 2025 analysis.

Transform complex venture capital reports into interactive experiences your team will actually read.

IPO Market Recovery: Tech vs. Biotech Divergence

The IPO market in 2025 presents a tale of two sectors. Technology companies have leveraged public market support to achieve their strongest IPO year since 2021, representing 95.1% of the value created through initial public offerings. Figma, Firefly Aerospace, Gemini, and Figure delivered strong Q3 listings, with September becoming the most active IPO month since 2021.

The PitchBook VC-Backed IPO Index has shown a positive trend, with tech IPOs particularly strong. Pricing outcomes improved sequentially through Q3, with most deals in August and September pricing above the midpoint of their marketed ranges. According to J.P. Morgan analysis included in the report, institutional investor demand remains robust for high-growth stories, and the IPO pipeline includes a large number of scaled, profitable, and high-growth companies encouraged by recent performance.

However, the picture for biotech is dramatically different. Through Q3, only eight pharma and biotech companies went public — sharply contrasting with 22 in 2024, itself well below the decade average of 39. The biotech sector faces a unique set of challenges: uncertainty around future NIH funding, potential price controls from the Most-Favored-Nation executive order, and rhetoric questioning drug-based care and vaccine effectiveness have collectively dampened market support.

Notably, roughly half of recent venture-backed tech IPOs priced at discounts to their latest private round, with conservative public peer discounts. While this may disappoint some private investors, it creates a healthier foundation for long-term aftermarket performance. The involvement of cornerstone investors in approximately one-quarter of Q3 IPOs also signals a maturing market.

Megadeals and Unicorn Valuations Surge

Megadeals have become the defining feature of venture capital trends in 2025. In Q3 alone, nine billion-dollar-plus financings accounted for nearly 40% of the quarter’s total deal value. VCs have averaged over 100 megadeals per quarter in 2025 — a level not seen since 2021 and 2022 — and these outsized rounds now account for 70% of yearly deal value.

The landmark deals illustrate the scale: Anthropic raised $13 billion in a Series F valuation at $183 billion — nearly triple its Series E valuation from just six months prior. xAI secured $10 billion in debt and equity at a $75 billion valuation, 50% higher than its previous round in November 2024. Databricks raised $1 billion at a $100 billion post-money valuation, a 61.3% increase from its Series J three months earlier. These velocity-of-value-creation numbers are extraordinary even by Silicon Valley standards.

The unicorn landscape has expanded dramatically. Active unicorn count continues to climb, with aggregate post-money valuation surpassing $3.7 trillion. Pre-money valuations have reached decade highs across all stages, from pre-seed through Series D+. However, many of these valuations remain private market marks that have yet to be tested in public markets, creating what some analysts describe as a valuation gap that could narrow as more companies seek exits.

Unlike previous years, most 2025 megadeals lack crossover investor participation — only 37% include crossovers, down from 60% in 2021 and 48% in 2022. This shift reflects the rise of megafunds and large VC firms gaining Registered Investment Advisor status, enabling them to make larger investments without needing mutual funds or hedge funds to co-invest. For context on how global financial institutions are navigating these dynamics, see the ECB Annual Report 2024.

Make sense of complex financial data — turn dense reports into engaging interactive experiences.

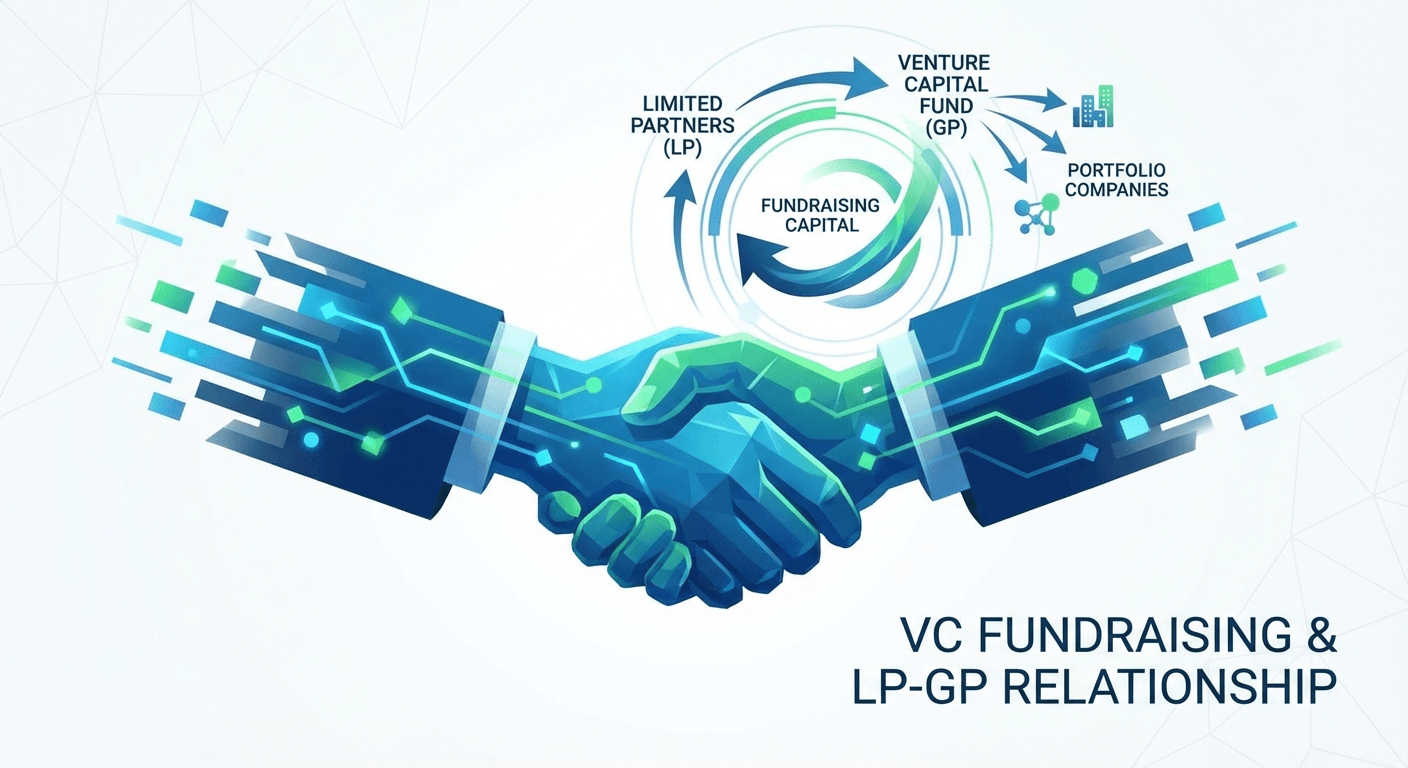

VC Fundraising Hits Multi-Year Lows

While deal activity surges, the fundraising side of venture capital tells a sobering story. Through Q3 2025, new LP commitments totaled only $45.7 billion — putting the year on pace for the lowest annual fundraising total since 2017. This disconnect between robust deployment and anemic fundraising creates a structural tension that cannot persist indefinitely.

The root cause is the liquidity crunch. VC distributions as a share of net asset value (NAV) have been improving — reaching 12.7% in recent quarters compared to a trough of 10.5% — but remain well below the long-term average. Limited partners who committed heavily during the 2020–2021 boom have received back far less than expected, making them reluctant to write new checks despite the opportunities they see in AI and other sectors.

General partners are responding by exploring alternative liquidity mechanisms. The use of secondaries continues to grow, with nearly 30% of secondary transactions in H1 2025 occurring at premiums to the most recent equity round — up from a low of 16% in H1 2023. Continuation-style vehicles are emerging as another tool for GPs to provide distributions while maintaining exposure to their best-performing portfolio companies.

The macro environment provides some tailwinds. The Federal Reserve lowered rates by 25 basis points in September, with J.P. Morgan projecting two more cuts before year-end and an additional cut in January 2026. Lower rates should support valuations and improve exit conditions, potentially unlocking the trapped capital that LPs desperately need. For related insights on financial stability, our Fed Financial Stability Report 2025 analysis provides broader context.

Exit Environment and M&A Acceleration

The venture capital exit landscape in 2025 is characterized by volume without the expected value recovery. While 2025 is on track for the second-highest number of completed exits ever, this metric is misleading: 75% of acquisitions occurred after companies reached only Series A, suggesting many of these are smaller acqui-hires or distressed sales rather than the large, value-creating exits that LPs need.

Large M&A activity tells a more optimistic story. VC-backed acquisitions valued at $500 million or more totaled 26 deals worth $36.5 billion through Q3, on pace to match or exceed recent years. The tech sector M&A revival has outpaced the broader market, with tailwinds from AI, cybersecurity, and consolidation driving activity. Big Tech companies are actively pursuing talent acquisitions and licensing deals to fill product gaps, particularly in AI where relatively nascent companies are being approached by strategics keen to add capabilities.

Private equity buyouts have quietly increased as well. PE firms are finding opportunities among VC-backed companies that have become profitable over recent years but cannot sustain the high growth that venture investors seek, aligning with the PE add-on strategy. This PE-VC convergence represents a meaningful new exit pathway for companies stuck in the “growth equity limbo.”

The secondaries market has also become an increasingly important liquidity mechanism. Secondary pricing has strengthened in line with broader private market trends, and startups founded in 2020 are seeing the most activity — coinciding with the typical four-year employee equity vesting period and the five-year Qualified Small Business Stock (QSBS) period.

Female Founders and Diversity in Venture Capital

The PitchBook NVCA report includes sobering data on female founders. Deal count for companies with at least one female founder is falling back to pre-2020 levels, with 2025 on track for approximately 3,095 deals compared to the 2021 peak of 5,233. All-female founding teams raised just $1.9 billion year-to-date — representing less than 1% of total venture capital invested.

The trend lines are moving in the wrong direction. The percentage of deals going to all-female teams is at its lowest since 2015, at 5.1% of deal count and 0.8% of deal value. Companies with at least one female founder captured 20.5% of deal count and 22.2% of deal value. First-time financings paint an even starker picture: 80% go to all-male teams, a ratio that has barely budged in a decade.

There is one bright spot: 2025 is pacing record venture-growth stage deals for female-founded startups, suggesting that the female-founded companies that do get funded are increasingly competitive at scale. The San Francisco-San Jose CSA has retaken the top spot for pre-seed and seed deals to all-female founder teams, followed by New York, Los Angeles, Boston, and Philadelphia.

Help your team digest critical market research — transform PDFs into interactive learning experiences.

Regional Venture Capital Spotlight

The geographic distribution of venture capital continues to concentrate heavily. In Q3 2025, the Bay Area captured 57% of all US venture capital value with $44 billion invested across 648 deals — a dominance that has only intensified with the AI boom, given that many leading AI companies are headquartered in San Francisco. New York followed with $9.6 billion across 469 deals, while Boston ($4.4 billion, 186 deals) and Los Angeles ($3.9 billion, 187 deals) rounded out the top four hubs.

The hub vs. non-hub dynamic is striking. Major venture hubs account for 73.4% of total deal value despite representing only 50.1% of deal count. At the venture-growth stage, the concentration is even more extreme: hubs capture 82% of deal value. Only at the early stage does the distribution become slightly more balanced, with non-hub markets accounting for 28.1% of value — though even this is driven by a handful of emerging ecosystems like Denver ($2 billion), Washington DC ($2 billion), and Miami ($0.8 billion).

The regional concentration of AI investment further exacerbates these geographic disparities. With AI companies representing the bulk of megadeals and the majority headquartered in San Francisco, the Bay Area’s share of total venture value is likely to remain elevated. For emerging hub cities, the opportunity lies in AI-adjacent sectors — defense tech, cybersecurity, climate tech, and healthcare AI — where geographic proximity to end customers or regulatory bodies matters more than proximity to foundation model labs.

NVCA Policy Highlights and Regulatory Shifts

The policy landscape for venture capital underwent significant changes in Q3 2025. The One Big Beautiful Bill Act (OBBBA), signed on July 4, delivered a mixed outcome for the venture community. Wins included leaving carried interest untouched, expanding the Qualified Small Business Stock (QSBS) exclusion with tiered structures and higher per-issuer caps, and making R&D expensing immediate and permanent — retroactively benefiting smaller firms from tax year 2022.

Capital markets reform saw progress with the DEAL Act advancing, offering greater flexibility for exempt reporting advisors handling secondaries and fund-of-fund structures. Legislation to expand the 3(c)(1) qualifying VC fund exemption — raising the investor cap to 500 LPs in early-stage funds — represents a significant modernization for capital formation. The venture community also secured a two-year delay in Anti-Money Laundering and Know Your Customer enforcement, pushing compliance deadlines past January 2026.

On the concerning side, the OBBBA accelerated the phaseout of energy tax credits, restructured the excise tax on university endowments, and removed the moratorium on AI-related tax proposals. Intellectual property pressures mounted as Commerce Secretary Lutnick advanced proposals to exercise “march-in rights” on university patents developed with federal funding and restructure USPTO fees. National security policy continues to evolve, with the National Defense Authorization Act discussions including provisions to restrict US investment in certain Chinese technologies. For insights on how global regulation is shaping tech markets, see our EU AI Act Regulation guide.

Frequently Asked Questions

What are the biggest venture capital trends in Q3 2025?

The biggest venture capital trends in Q3 2025 include AI and machine learning dominating 64.3% of deal value, a resurgence of megadeals with nine billion-dollar-plus financings in a single quarter, the IPO market showing recovery led by tech companies, and fundraising heading toward its lowest commitment total since 2017 due to an ongoing liquidity crunch for limited partners.

How much did VCs invest in Q3 2025?

In Q3 2025, venture capital firms deployed $80.9 billion across approximately 4,208 deals, representing a 4.9% quarter-over-quarter increase in deal value. Year-to-date 2025 deal value already surpassed the full-year totals of 2022, 2023, and 2024.

Why is AI dominating venture capital investment?

AI dominates venture capital because companies racing to meet soaring demand need significant funding for talent acquisition, chip procurement, and infrastructure buildout. In 2025, AI accounted for 64.3% of all VC deal value despite only 37.5% of deal count, with companies like Databricks, Anthropic, and xAI raising multi-billion dollar rounds.

What is the venture capital fundraising outlook for 2025?

VC fundraising in 2025 is heading toward its lowest annual commitment total since 2017, with only $45.7 billion through Q3. Limited partners face a liquidity crunch as distributions remain below historical averages, discouraging reinvestment despite strong deal activity driven by AI.

How is the IPO market performing for VC-backed companies?

The IPO market is recovering unevenly. Tech companies had their strongest IPO year since 2021, representing 95.1% of IPO value, with strong listings from Figma, Firefly Aerospace, and Gemini. However, biotech IPOs declined sharply to just eight through Q3, compared to 22 in 2024.