—

0:00

PwC Global CEO Survey 2025: Key Findings on AI, Climate & Business Reinvention

Table of Contents

- PwC CEO Survey 2025: The Definitive Pulse Check on Global Business Leadership

- Generative AI Impact: Early Returns and Rising Expectations

- CEO AI Integration Priorities: Technology Platforms Lead, Workforce Skills Lag

- Climate Investment Returns: The Business Case Strengthens

- The Viability Crisis: Why 40% of CEOs Fear Obsolescence

- Trust as a Barrier to AI Adoption

- Economic Outlook and CEO Confidence Trends

- Sector Disruption: Cross-Industry Competition Intensifies

- The Reinvention Imperative: Barriers and Solutions

- Implications for Strategic Planning and Investment Decisions

🔑 Key Takeaways

- PwC CEO Survey 2025: The Definitive Pulse Check on Global Business Leadership — PwC’s 28th Annual Global CEO Survey, subtitled “Reinvention on the Edge of Tomorrow,” delivers the most comprehensive view of chief executive sentiment and strategy available anywhere.

- Generative AI Impact: Early Returns and Rising Expectations — The PwC CEO Survey 2025 provides the most authoritative data available on the real-world impact of generative AI on enterprise performance.

- CEO AI Integration Priorities: Technology Platforms Lead, Workforce Skills Lag — The PwC CEO Survey 2025 reveals a telling hierarchy in how chief executives plan to integrate AI over the next three years.

- Climate Investment Returns: The Business Case Strengthens — One of the most impactful findings of the PwC CEO Survey 2025 is the growing evidence that climate-friendly investments are paying off financially.

- The Viability Crisis: Why 40% of CEOs Fear Obsolescence — Perhaps the most striking finding in the PwC CEO Survey 2025 is the persistent existential anxiety among global CEOs.

PwC CEO Survey 2025: The Definitive Pulse Check on Global Business Leadership

PwC’s 28th Annual Global CEO Survey, subtitled “Reinvention on the Edge of Tomorrow,” delivers the most comprehensive view of chief executive sentiment and strategy available anywhere. Based on responses from 4,701 CEOs representing every region of the global economy, the 2025 survey captures a business landscape shaped by two defining forces: the rapid adoption of generative AI and the accelerating imperative of climate action. The findings reveal a stark divide between organizations moving aggressively to capture value from these forces and those constrained by inertia.

The survey’s central tension is captured in William Gibson’s famous observation: “The future is already here—it’s just not evenly distributed.” Some CEOs are investing decisively in generative AI, realizing early returns on climate-friendly investments, and reinventing their business models for a fundamentally different competitive landscape. Yet many others are moving slowly, constrained by leadership mindsets, weak decision-making processes, and institutional resistance to change. For this latter group, the survey delivers an uncomfortable message: incremental adjustments to existing models may not be sufficient to ensure long-term viability.

The macroeconomic outlook provides a cautiously optimistic backdrop. Nearly 60% of CEOs expected global economic growth to increase over the next 12 months—up dramatically from 38% in the previous year’s survey and only 18% two years ago. By a ratio of more than two to one, CEOs expect to increase rather than decrease headcount (42% vs. 17%) in the year ahead. This near-term optimism, however, exists in sharp tension with deep concerns about long-term viability, creating a paradox that defines the current strategic moment.

Generative AI Impact: Early Returns and Rising Expectations

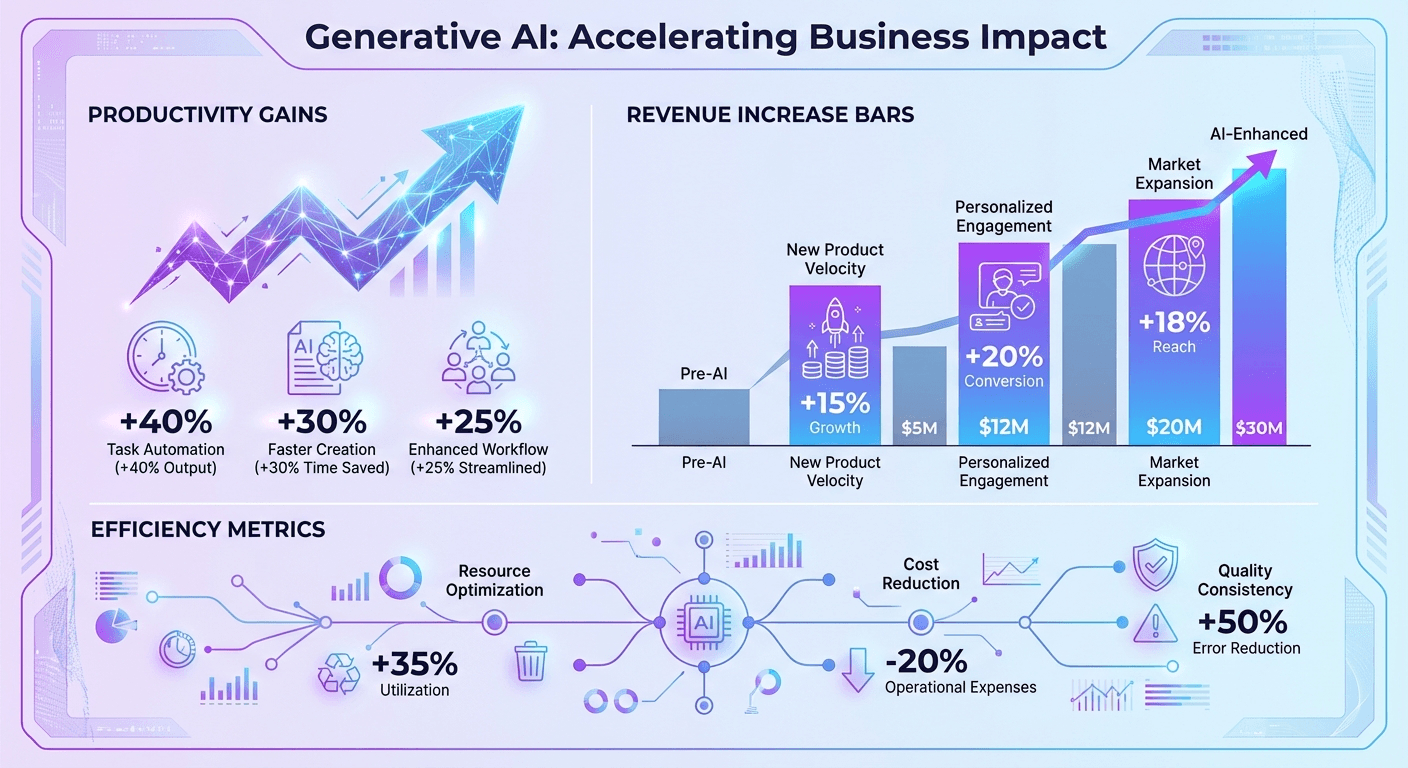

The PwC CEO Survey 2025 provides the most authoritative data available on the real-world impact of generative AI on enterprise performance. Only two years after GenAI appeared on most executives’ radar, the results show that companies worldwide are adopting it at scale—and many are already seeing measurable returns.

More than half of CEOs (56%) report that GenAI has resulted in efficiencies in how employees use their time, the most widely cited benefit. Around one-third report increased revenue (32%) and profitability (34%). These outcomes are slightly below the expectations CEOs shared a year earlier, but this gap has not dampened optimism. CEO expectations for GenAI impacts in the year ahead are remarkably similar to those reported in last year’s survey, with 49% expecting GenAI to increase profitability over the next 12 months.

Perhaps most notably, the employment impact of GenAI contradicts the widespread narrative of AI-driven job destruction. While 13% of CEOs report reducing headcount due to GenAI, a slightly higher percentage (17%) say headcount has increased as a result of GenAI investments. Companies in insurance, retail, pharmaceuticals, and life sciences were most likely to have made cuts (16%), but the overall picture suggests that GenAI is currently creating more jobs than it eliminates. This finding aligns with the broader analysis in our coverage of the McKinsey State of AI 2024 report, which similarly finds that AI adoption is driving workforce expansion alongside efficiency gains.

CEO AI Integration Priorities: Technology Platforms Lead, Workforce Skills Lag

The PwC CEO Survey 2025 reveals a telling hierarchy in how chief executives plan to integrate AI over the next three years. Almost half of CEOs (47%) identify integrating AI into technology platforms as their top priority, followed by business processes and workflows (41%). Fewer are prioritizing AI for new product and service development (30%) or reshaping core business strategy (24%).

Most concerning is that only 31% of CEOs are planning to systematically integrate AI into workforce and skills strategy. The survey identifies this as a potential strategic misstep, noting that “realising the potential of GenAI will depend on employees knowing when and how to use AI tools in their work—and understanding the potential pitfalls.” This workforce skills gap could become the critical bottleneck that prevents organizations from capturing the full productivity potential of their AI investments.

The survey’s recommendation is direct: capturing GenAI’s productivity potential will soon be “table stakes” in many industries. This requires a systematic approach encompassing data readiness, technology platform integration, workflow redesign, and—crucially—comprehensive workforce skills programs. Organizations that build this foundation will also be positioned to seize the larger opportunities ahead, whether transforming specific functions or undertaking more dramatic business model changes. Our analysis of the Accenture Technology Vision 2025 reinforces this finding, highlighting that enterprises leading in AI adoption are those investing equally in technology and human capabilities.

📊 Explore this analysis with interactive data visualizations

Climate Investment Returns: The Business Case Strengthens

One of the most impactful findings of the PwC CEO Survey 2025 is the growing evidence that climate-friendly investments are paying off financially. When CEOs were asked to assess the financial impact of their climate investments over the past five years, the results were unequivocal: these investments were six times more likely to have increased revenue than decreased it.

Specifically, one-third of CEOs (33%) report increased revenue from climate-friendly investments, while only 5% report decreased revenue. Two-thirds say these investments either reduced costs (18%) or had no significant cost impact (42%). After adjusting for geography and other factors, PwC finds that making climate-friendly investments is associated with higher profit margins—consistent with analysis from the previous year’s survey and supporting Harvard Business School research showing faster revenue growth among firms transitioning toward climate solutions.

The geographic distribution of these returns is notable. CEOs in Mainland China are significantly more likely to report additional revenues from climate investments (60%) and government incentives received (46%) compared to other regions. European CEOs, particularly in Germany and France, are more likely to report increased costs (around 50%), while US CEOs report lower cost impacts (around 20%). These regional variations reflect the different mix of incentives, regulations, and market conditions that shape the climate investment landscape. Crucially, the overall global trend is positive: climate action is not a cost of doing business but increasingly a driver of competitive advantage.

The Viability Crisis: Why 40% of CEOs Fear Obsolescence

Perhaps the most striking finding in the PwC CEO Survey 2025 is the persistent existential anxiety among global CEOs. Consistent with the previous year’s survey, four in ten CEOs believe their company will no longer be viable in ten years if it continues on its current path. This is not peripheral pessimism—it represents the considered judgment of nearly half the world’s most powerful business leaders about the sufficiency of their current strategies.

The drivers of this concern are structural. Nearly 40% of CEOs report that their companies started competing in new sectors over the past five years, indicating that sector boundaries are blurring at an unprecedented rate. Technology companies are entering financial services, healthcare organizations are becoming data platforms, and energy companies are reinventing themselves around climate solutions. This cross-sector competition means that competitive threats can emerge from unexpected directions, rendering traditional competitive moats less effective.

Despite this awareness, the pace of reinvention remains alarmingly slow. On average, only 7% of revenue over the last five years has come from distinct new businesses added by organizations during that period. The survey identifies three key barriers to faster reinvention: weak decision-making processes that favor incrementalism, low levels of resource reallocation from year to year (organizational inertia), and a fundamental mismatch between the short expected tenure of many CEOs and the long-term nature of the megatrends reshaping their industries.

Trust as a Barrier to AI Adoption

The PwC CEO Survey 2025 identifies trust as a significant hurdle to broader GenAI adoption across organizations. While the technology’s potential is widely recognized and early adopters are seeing tangible results, the diffusion of AI throughout organizational processes requires stakeholders—employees, customers, regulators, and boards—to trust that AI systems will perform reliably, ethically, and transparently.

The trust challenge operates at multiple levels. At the employee level, concerns about job displacement, decision transparency, and the reliability of AI-generated outputs create resistance to adoption. At the customer level, questions about data privacy, the accuracy of AI-driven recommendations, and the loss of human interaction in service delivery can slow commercial deployment. At the regulatory level, evolving AI governance frameworks create compliance uncertainty that makes organizations cautious about expanding AI use cases.

Building trust in AI requires deliberate organizational effort. The survey suggests that organizations achieving the highest AI adoption rates are those investing in governance frameworks, employee education programs, and transparent communication about how AI is being used and what safeguards are in place. For organizations navigating the trust dimension of AI adoption, our analysis of the AI alignment taxonomy provides essential framework for understanding how to build trustworthy AI systems. The interplay between technical capability and organizational trust may ultimately determine which companies successfully capture AI’s value and which remain trapped in the pilot phase.

📊 Explore this analysis with interactive data visualizations

Economic Outlook and CEO Confidence Trends

The PwC CEO Survey 2025 captures a notable shift in economic sentiment among global business leaders. Nearly 60% of CEOs expected global economic growth to increase over the next 12 months—a dramatic improvement from 38% in the prior year and only 18% two years ago. This rising optimism reflects improved macroeconomic conditions, resilient consumer spending in key markets, and growing confidence in the ability to monetize technology investments, particularly in AI.

Headcount expectations reinforce this positive outlook. By a ratio of more than two to one, CEOs plan to increase rather than decrease employment (42% vs. 17%) in the year ahead. This commitment to workforce expansion, occurring alongside rising AI adoption, suggests that CEOs see AI as augmenting rather than replacing human capabilities in the near term. The combination of technological investment and workforce growth points to an expansion-oriented strategy across much of the global economy.

However, the survey reveals a troubling disconnect between short-term optimism and long-term concern. CEOs are simultaneously confident about near-term growth while deeply worried about their companies’ ten-year viability. This paradox suggests that many CEOs are prioritizing immediate performance—driven by quarterly earnings expectations and short-term incentive structures—while recognizing that structural changes requiring multi-year investment are necessary for long-term survival. Resolving this temporal mismatch is one of the central leadership challenges identified by the survey.

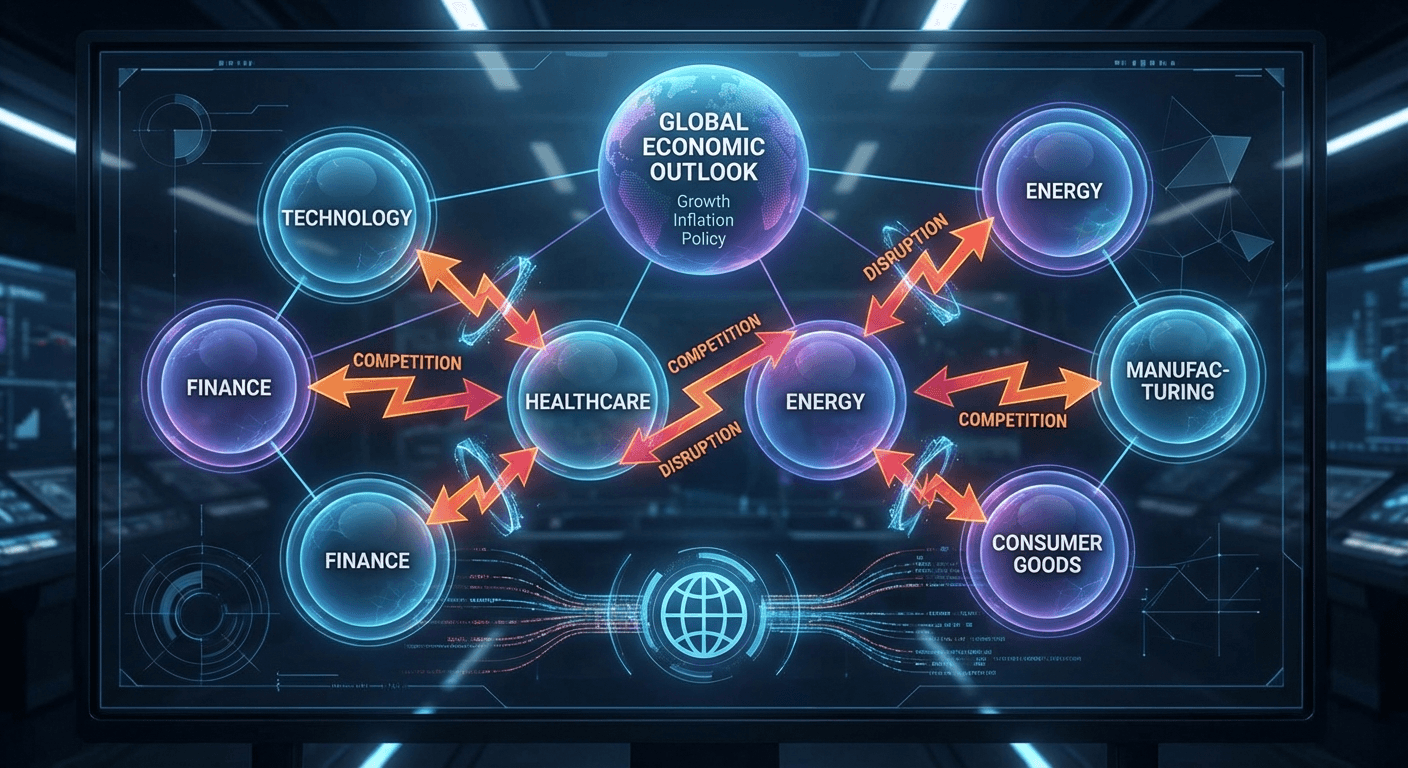

Sector Disruption: Cross-Industry Competition Intensifies

The PwC CEO Survey 2025 quantifies a trend that has been reshaping competitive landscapes: the blurring of sector boundaries. Nearly 40% of CEOs report that their companies started competing in new sectors over the past five years, driven by digital transformation, AI capabilities, and the convergence of previously distinct industries. This cross-sector competition is accelerating and intensifying as technology reduces traditional barriers to entry, a trend also documented in the World Economic Forum Global Risks Report 2025.

Financial services illustrates this trend clearly. Technology companies are offering banking, payments, and investment services; healthcare organizations are building data platforms that compete with traditional analytics providers; and retailers are developing financial products for their customer base. Conversely, financial institutions are expanding into technology services, health data management, and sustainability consulting. The result is a competitive landscape where industry classification provides decreasing strategic value and competitive threats emerge from unexpected directions.

For organizations assessing their competitive positioning, the PwC CEO Survey data suggests that sector-specific strategies may be insufficient. Instead, companies need to develop capabilities—in AI, data analytics, platform economics, and customer experience—that transcend traditional industry boundaries. Our analysis of the BCG Global Asset Management Report 2024 illustrates how this dynamic is specifically reshaping the financial services industry, where asset managers increasingly compete with technology platforms and alternative data providers.

The Reinvention Imperative: Barriers and Solutions

The gap between the recognition of the need for reinvention and the execution of reinvention represents the core strategic challenge identified by the PwC CEO Survey 2025. While 40% of CEOs acknowledge their companies’ current path is unsustainable, only 7% of revenue comes from genuinely new businesses—a pace of transformation that is fundamentally insufficient to address the scale of disruption underway.

The survey identifies three structural barriers that explain this reinvention gap. First, weak decision-making processes that favor incremental improvements over transformational bets. Many organizations lack the governance structures needed to evaluate, fund, and nurture genuinely new business models alongside their established operations. Second, low resource reallocation from year to year. Organizational inertia means that budgets, talent, and management attention remain concentrated on existing businesses even when the data clearly supports investment in new areas. Third, a CEO tenure mismatch—the average CEO tenure of five to seven years creates incentive structures that favor near-term performance over the long-term investments needed to navigate megatrend-driven disruption.

Addressing these barriers requires changes in corporate governance, executive incentive design, and organizational culture. The survey suggests that the most successful reinventors are those with boards that actively challenge management’s strategic assumptions, incentive structures that reward long-term value creation alongside short-term performance, and organizational cultures that tolerate the ambiguity and risk inherent in building genuinely new businesses. For companies looking to benchmark their reinvention efforts, the Financial Services Regulatory Outlook 2026 analysis provides perspective on how regulatory frameworks are evolving to both enable and constrain strategic transformation across industries.

Implications for Strategic Planning and Investment Decisions

The PwC CEO Survey 2025 delivers actionable insights for multiple audiences. For corporate strategists, the data makes an overwhelming case for accelerating AI integration—not as a technology project but as a business transformation initiative that spans technology platforms, business processes, workforce capabilities, and core strategy. The finding that only 24% of CEOs plan to systematically integrate AI into core business strategy represents a strategic vulnerability for the majority.

For investors and analysts, the survey provides a framework for evaluating management quality. Companies whose leaders are investing in AI with a comprehensive strategy—covering technology, processes, workforce skills, and business model innovation—are more likely to capture the disproportionate returns that accrue to early movers. Similarly, the demonstrated link between climate-friendly investments and higher profit margins suggests that sustainability commitment is a leading indicator of management quality and long-term value creation potential.

For boards and governance professionals, the survey highlights the urgency of addressing the reinvention gap. The disconnect between CEO awareness of existential risk (40% believe their company won’t be viable in 10 years) and the pace of actual transformation (7% of revenue from new businesses) suggests that current governance mechanisms are not effectively translating strategic awareness into organizational action. Boards must challenge whether their oversight, incentive structures, and resource allocation processes are fit for an era of accelerating disruption, as highlighted in our Meta Platforms 10-K 2024 analysis of how leading technology companies are structuring governance for the AI era.

📊 Explore this analysis with interactive data visualizations

Frequently Asked Questions

What are the key findings of the PwC Global CEO Survey 2025?

The PwC 28th Annual Global CEO Survey 2025, based on 4,701 CEO responses worldwide, reveals that one-third of CEOs report GenAI has already increased revenue and profitability, climate investments are paying off with 6x more likely to increase rather than decrease revenue, nearly 40% of companies now compete in new sectors, and 4 in 10 CEOs believe their company won’t be viable in 10 years without change.

What do CEOs say about generative AI impact on business?

56% of CEOs report GenAI has created efficiencies in employee time, 34% report increased profitability, and 32% report increased revenue. Looking ahead, 49% expect GenAI to increase profitability in the next 12 months. Top priorities include integrating AI into technology platforms (47%) and business processes (41%), though only 31% plan to integrate AI into workforce skills.

How are climate investments performing according to the PwC CEO Survey?

Climate-friendly investments are 6x more likely to have increased revenue than decreased it. One-third of CEOs report increased revenue from climate investments, while two-thirds say these investments either reduced costs or had no significant cost impact. After adjusting for geography, climate investments are associated with higher profit margins.

What percentage of CEOs think their company will be viable in 10 years?

Consistent with the prior year’s survey, 4 in 10 CEOs (40%) believe their company will no longer be viable in ten years if it continues on its current path. This highlights the urgency for business reinvention, yet on average only 7% of revenue over the past five years has come from distinct new businesses, indicating slow reinvention pace.

How many CEOs participated in the PwC 2025 Global CEO Survey?

The PwC 28th Annual Global CEO Survey 2025 is based on responses from 4,701 chief executives representing every region of the world economy. The survey covers topics including generative AI adoption, climate investment returns, sector disruption, business reinvention, and economic outlook.