—

0:00

PwC Global Investor Survey 2025: Key Findings on AI, Risk, and Resilience

Table of Contents

- Global Investor Survey 2025: The Investment Landscape Shifts

- Macroeconomic Outlook: Why Investors Expect Modest Growth in 2026

- AI Investment Priorities: Technological Transformation Leads Capital Allocation

- Cybersecurity and Risk: The Investor View on Digital Defense

- Cross-Sector Expansion: How Industry Convergence Drives Investor Value

- Business Model Agility and Investor Expectations for 2026

- Sustainability and ESG: Investor Demand for Transparent Reporting

- Information Sources: How Global Investors Make Investment Decisions

- Capital Allocation Strategies: Where the Smart Money Is Flowing

- Investor Governance: Building Trust Through Transparency

🔑 Key Takeaways

- Global Investor Survey 2025: The Investment Landscape Shifts — The PwC Global Investor Survey 2025 captures a pivotal moment in global finance.

- Macroeconomic Outlook: Why Investors Expect Modest Growth in 2026 — One of the most striking findings from the PwC Global Investor Survey 2025 is the decidedly cautious macroeconomic outlook.

- AI Investment Priorities: Technological Transformation Leads Capital Allocation — Technology investment has emerged as the undisputed priority in the PwC Global Investor Survey 2025.

- Cybersecurity and Risk: The Investor View on Digital Defense — Cybersecurity has surged to the top of investor concerns, with 55% of respondents identifying cyber risks as the primary threat to the companies they invest in or cover.

- Cross-Sector Expansion: How Industry Convergence Drives Investor Value — A fascinating finding from the PwC Global Investor Survey 2025 is the growing investor appetite for cross-sector business models.

Global Investor Survey 2025: The Investment Landscape Shifts

The PwC Global Investor Survey 2025 captures a pivotal moment in global finance. Conducted between September and October 2025, this comprehensive study gathered insights from 1,074 investment professionals spanning 26 countries, representing institutions with a median of $75 billion in assets under management. The survey paints a clear picture: investors are no longer content with incremental improvement—they demand strategic reinvention anchored in technology and resilience.

The backdrop for this survey is a global economy caught between competing forces. Inflation, while easing in many markets, remains a persistent concern for 44% of respondents. Geopolitical tensions continue to reshape supply chains and capital flows. Yet amid this uncertainty, investors see enormous opportunity in companies willing to embrace transformative technologies and adapt their business models. The central thesis from PwC’s research is encapsulated in their tagline: “Resilience first, innovation always.”

This isn’t merely a sentiment—it’s a capital allocation directive. Investors are actively steering hundreds of billions of dollars toward companies that can demonstrate both defensive positioning and offensive capability through technology. Understanding these priorities is essential for any executive, fund manager, or asset management professional navigating the 2026 investment landscape.

Macroeconomic Outlook: Why Investors Expect Modest Growth in 2026

One of the most striking findings from the PwC Global Investor Survey 2025 is the decidedly cautious macroeconomic outlook. Less than a third of respondents anticipate global GDP growth exceeding 2% over the next 12 months. This tempered expectation reflects a mature assessment of the headwinds facing the global economy—from sticky core inflation in major economies to the drag of higher-for-longer interest rates on capital-intensive sectors.

Breaking down the numbers, only 2% of investors expect the economy to “improve significantly,” while 26% predict moderate improvement and 33% foresee slight improvement. Meanwhile, 18% expect the economy to remain static, and 20% anticipate some form of decline. This distribution reveals a market consensus that has shifted decisively away from the post-pandemic recovery euphoria toward pragmatic realism.

For institutional investors, this outlook has profound portfolio implications. The emphasis shifts from chasing cyclical growth to identifying companies with structural advantages—those investing in technology, building operational resilience, and managing interconnected risks. As documented in the Goldman Sachs 2024 analysis, this defensive positioning combined with selective innovation is becoming the dominant institutional investment thesis.

The implications extend beyond traditional equity markets. Fixed-income investors (64% of survey respondents), private equity specialists (33%), and even sovereign wealth funds are recalibrating their expectations. The consensus is clear: companies that can deliver consistent returns in a low-growth environment—through operational efficiency, technological leverage, and strategic agility—will command premium valuations.

AI Investment Priorities: Technological Transformation Leads Capital Allocation

Technology investment has emerged as the undisputed priority in the PwC Global Investor Survey 2025. A commanding 64% of investors want companies to increase capital allocation to technological transformation—the highest priority across all categories surveyed. This represents more than a trend; it signals a fundamental reorientation of how institutional money views corporate spending.

The investor mandate is clear: deploy AI at enterprise scale, but do it with measurable outcomes. Respondents aren’t satisfied with pilot programs and innovation labs—they want to see generative AI and advanced analytics embedded in core business processes, driving measurable improvements in revenue, margins, and competitive positioning. Companies that can demonstrate concrete ROI from their AI investments are rewarded; those still in experimental mode face increasing scrutiny.

Interestingly, the survey reveals a nuanced view of AI as simultaneously an opportunity and a risk. Technological disruption ranks as the second-highest threat at 53%, right behind cybersecurity at 55%. Investors understand that AI creates winners and losers—companies that harness it effectively gain enormous advantages, while laggards face existential competitive pressure. This duality explains why investors simultaneously push for more technology spending while demanding robust governance frameworks for AI deployment.

The implications for corporate strategy are significant. CFOs and CIOs must frame technology investments not as cost centers but as strategic imperatives with clear milestones and KPIs. Investors want to see technology roadmaps tied to financial outcomes, with regular reporting on progress. As explored in our analysis of McKinsey’s State of AI research, the gap between AI leaders and laggards is widening rapidly, and investors are pricing this differential into their models.

📊 Explore this analysis with interactive data visualizations

Cybersecurity and Risk: The Investor View on Digital Defense

Cybersecurity has surged to the top of investor concerns, with 55% of respondents identifying cyber risks as the primary threat to the companies they invest in or cover. This marks a significant escalation from previous surveys and reflects the reality that digital transformation—while essential—dramatically expands the attack surface for enterprises.

The PwC survey reveals that 49% of investors want companies to increase their cybersecurity spending, making it the second-highest capital allocation priority. This isn’t just about defending against attacks—it’s about building the trust infrastructure that enables digital business models. Investors recognize that a major cyber breach can destroy shareholder value overnight, making cybersecurity a fundamental component of enterprise risk management.

What makes the 2025 findings particularly notable is the interconnection investors see between cyber risk and other threats. Geopolitical conflict (42%), for instance, is increasingly manifested through state-sponsored cyber warfare and technology supply chain disruption. Similarly, the rapid deployment of AI systems creates new attack vectors that require sophisticated defensive capabilities. For investors, cybersecurity is no longer a line item in the IT budget—it’s a board-level strategic priority that directly impacts long-term value creation.

The survey also highlights the growing importance of cybersecurity governance. Investors want to see dedicated board oversight, regular penetration testing, incident response capabilities, and transparent disclosure practices. Companies that treat cybersecurity as a competitive advantage—not just a compliance requirement—are better positioned to attract institutional capital. The banking risk management landscape offers valuable parallels, as financial institutions have been at the forefront of integrating cybersecurity into enterprise risk frameworks.

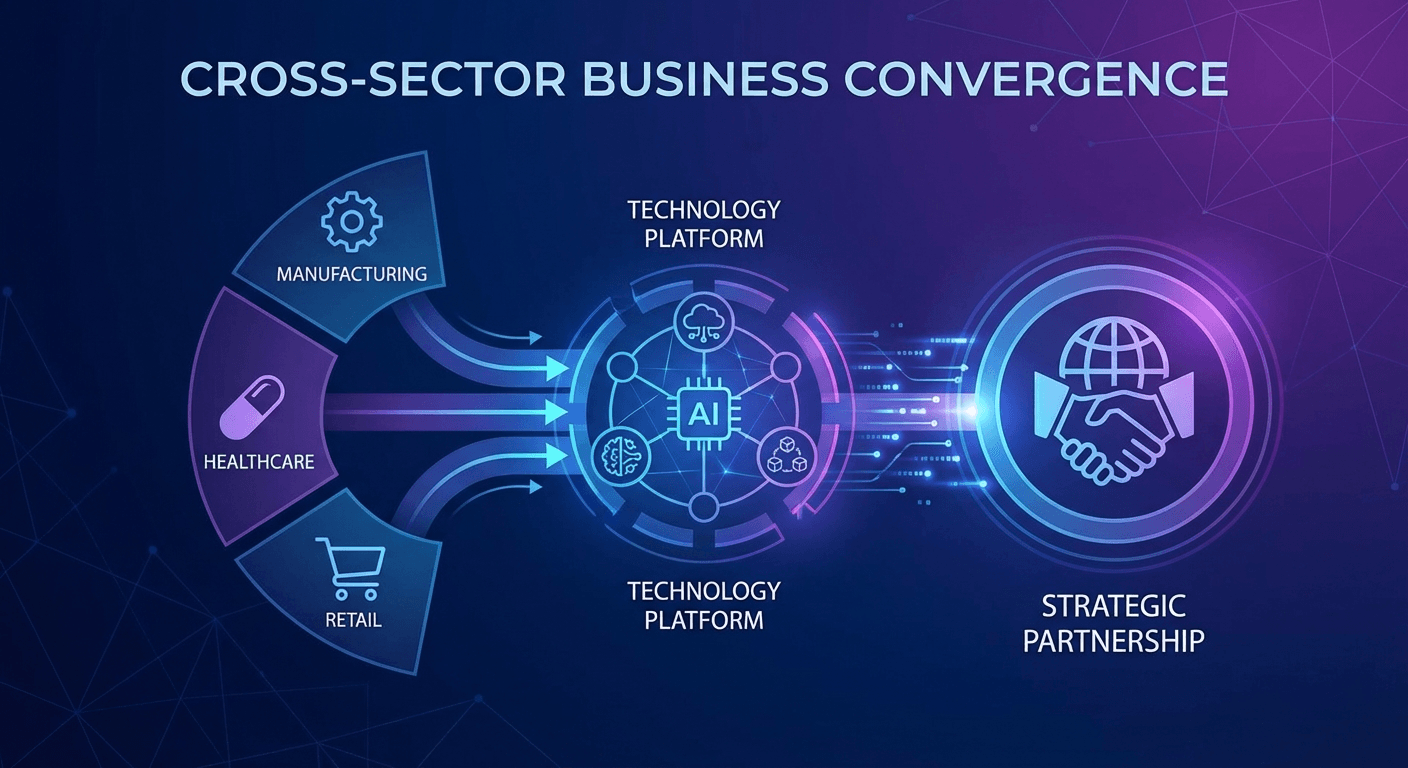

Cross-Sector Expansion: How Industry Convergence Drives Investor Value

A fascinating finding from the PwC Global Investor Survey 2025 is the growing investor appetite for cross-sector business models. When presented with a scenario comparing a focused, single-sector company to one expanding across traditional industry boundaries, investors increasingly favored the cross-sector approach. This preference challenges decades of investment wisdom that rewarded “pure-play” business models with clear sector definitions.

The logic behind this shift is compelling. As technology platforms enable companies to compete in adjacent markets—think Amazon moving from e-commerce to cloud computing to healthcare, or Apple expanding from devices into financial services—investors recognize that sector boundaries are increasingly artificial. Companies that leverage their technological and data advantages across multiple sectors can build deeper competitive moats, diversify revenue streams, and capture more of the value chain.

However, investors aren’t endorsing reckless diversification. The PwC survey makes clear that cross-sector expansion must be technology-driven and strategic, not opportunistic. Investors want to see a clear rationale for how entering new sectors creates synergies with existing capabilities, how technology platforms enable efficient multi-sector operations, and how management teams will maintain execution quality across a broader operational footprint.

For companies considering cross-sector moves, the message is clear: build the technological foundation first, then expand strategically. Investors will reward companies that demonstrate how their technology platforms, data assets, and operational capabilities can create value across traditional industry lines, while punishing those that diversify without a clear strategic logic.

Business Model Agility and Investor Expectations for 2026

Business model agility ranks as a critical priority in the PwC Global Investor Survey 2025, with 48% of investors calling for increased investment in this area. This reflects a recognition that static business models—no matter how successful historically—are vulnerable to disruption in an era of accelerating technological change and geopolitical volatility.

Investors define agility across several dimensions: the ability to pivot product offerings in response to market shifts, the capability to rapidly integrate new technologies into existing operations, and the organizational flexibility to reallocate resources across business units as opportunities emerge. Companies that demonstrate these capabilities are rewarded with higher valuation multiples, as investors price in their superior ability to navigate uncertainty.

The survey data reveals that agility is closely linked to technology investment. Companies with strong digital infrastructure can reconfigure their operations faster, test new business models with lower capital commitment, and scale successful experiments more efficiently. This creates a virtuous cycle where technology investment enables agility, which in turn drives competitive advantage and superior returns.

Regulatory compliance and adaptation also features prominently, with 41% of investors wanting increased investment in this area. As analyzed in the Financial Services Regulatory Outlook 2026, the evolving regulatory landscape—particularly around AI governance, data privacy, and ESG disclosure—requires proactive investment in compliance capabilities that can adapt to changing requirements without disrupting core operations.

📊 Explore this analysis with interactive data visualizations

Sustainability and ESG: Investor Demand for Transparent Reporting

The PwC Global Investor Survey 2025 reveals a nuanced picture of investor attitudes toward sustainability. While only 39% to 45% of investors say they rely heavily on sustainability disclosures and materiality assessments for risk and opportunity evaluation, a remarkable 78% believe that providing sustainability information has a positive impact on investor engagement. This gap between reliance and perceived value suggests that ESG reporting is transitioning from a nice-to-have to a baseline expectation.

The data shows that investors use sustainability information differently depending on their focus. Climate change concerns 25% of respondents as a high or extreme threat, while social inequality registers at 16%. These relatively modest figures compared to cyber and technology risks suggest that sustainability is increasingly viewed through a financial materiality lens rather than as a standalone ethical imperative.

For companies, the implications are clear: sustainability reporting must be integrated into financial narratives, not siloed in separate reports. Investors want to understand how climate risks affect cash flows, how social capital investments drive productivity, and how governance structures ensure long-term value creation. The most effective sustainability disclosures are those that connect ESG metrics directly to financial performance and strategic objectives.

Supply chain management (21% wanting increased allocation) and human capital management (19%) also feature in investor priorities, reflecting a broadening view of what constitutes material sustainability factors. As stakeholder expectations evolve and regulatory frameworks like ESRS in Europe take effect, companies that proactively build comprehensive sustainability reporting capabilities will have a significant advantage in attracting institutional capital.

Information Sources: How Global Investors Make Investment Decisions

The PwC Global Investor Survey 2025 offers valuable insights into how institutional investors consume and prioritize information. Traditional sources remain dominant: analyst reports are used extensively by 21% of respondents, while credit ratings agencies (18%) and third-party data sources (18%) maintain their central role in investment decision-making. This persistence of traditional information channels underscores the premium investors place on credibility and methodological rigor.

However, the survey also captures the emergence of new information sources. Generative AI is being used by 9% of investors to a very large extent and by 25% to a large extent, indicating rapid adoption of AI-powered research tools. Alternative data sources show similar adoption patterns, with investors increasingly leveraging satellite imagery, web scraping, social media sentiment, and transaction data to gain informational edges.

The message for companies is clear: while traditional financial reporting and analyst coverage remain essential, the information ecosystem is diversifying rapidly. Companies need to ensure their stories are accessible across multiple channels—from structured data feeds for quantitative investors to clear narrative disclosures for fundamental analysts. The emphasis on structured data and machine-readable disclosures from regulators like the SEC will only accelerate this trend.

Social media, interestingly, remains at the bottom of investor information sources, with only 4% using it to a very large extent. This suggests that while social media can move markets in the short term, institutional investors still overwhelmingly rely on verified, structured information for their long-term allocation decisions. Companies should focus their investor communication efforts on quality and depth rather than social media reach.

Capital Allocation Strategies: Where the Smart Money Is Flowing

The PwC Global Investor Survey 2025 provides a comprehensive roadmap of investor capital allocation preferences. Beyond the headline figures on technology (64%) and cybersecurity (49%), the survey reveals a sophisticated hierarchy of investment priorities that offers actionable intelligence for corporate strategists and portfolio managers.

Business model agility (48%) rounds out the top three, followed by regulatory compliance (41%), supply chain management (21%), human capital management (19%), stakeholder management (19%), and climate adaptation (15%). Notably, very few investors want to see decreased allocation in any category—the dominant sentiment is that companies need to invest more, not less, across virtually all strategic dimensions. The question is one of prioritization, not reduction.

The survey’s geographic dimension adds further nuance. With 72% of respondents investing in the US, followed by the UK (55%), Germany (46%), France (39%), and Canada (37%), capital allocation preferences reflect a distinctly transatlantic perspective. Technology and media companies receive disproportionate investor attention, with 87% of respondents investing in the TMT sector, followed by financial services (52%) and consumer markets (51%).

For portfolio constructors, these findings suggest that the winning investment thesis for 2026 combines technology-led transformation with risk-aware governance. As IMF global economic projections continue to emphasize uncertainty, companies that can demonstrate both innovation capability and operational resilience will command premium valuations in global capital markets.

Investor Governance: Building Trust Through Transparency

Governance emerges as a critical differentiator in the PwC Global Investor Survey 2025. Investors aren’t just looking at what companies invest in—they’re scrutinizing how those investments are governed, measured, and communicated. The survey’s finding that investors want “numbers they can test, governance they can understand, and a narrative that connects strategy to cash flows” encapsulates this governance imperative.

This emphasis on governance extends to AI deployment specifically. As companies rush to implement generative AI across their operations, investors want assurance that these deployments are governed by robust frameworks covering data privacy, algorithmic bias, intellectual property, and operational risk. Companies that can demonstrate responsible AI governance are more likely to receive investor support for continued technology investment.

The planned investment horizon data provides additional context. With 37% of respondents on 3-5 year horizons and 32% on 2 years or less, investors are balancing near-term performance expectations with longer-term transformation timelines. This creates tension for companies that need to deliver quarterly results while investing in multi-year technology transformations. Effective governance—including clear milestone reporting and transparent communication about trade-offs—helps bridge this temporal gap. The EBA Risk Assessment Report 2025 provides complementary perspective on how governance frameworks are evolving across regulated industries.

📊 Explore this analysis with interactive data visualizations

Frequently Asked Questions

What are the key findings of the PwC Global Investor Survey 2025?

The PwC Global Investor Survey 2025 reveals that investors prioritize technological transformation (64% want increased allocation), cybersecurity (49%), and business model agility (48%). Less than a third expect global GDP growth above 2%, with cyber risks (55%) and technological disruption (53%) seen as the top threats. Investors increasingly favor cross-sector business models and demand transparent AI governance.

How are investors allocating capital to AI and technology in 2025?

According to the PwC survey, 64% of investors want companies to increase capital allocation to technological transformation, while 49% call for more cybersecurity spending. Investors see AI as both an opportunity and a risk, with emphasis on enterprise-wide AI deployment, measurable ROI metrics, and responsible AI governance frameworks that address bias, privacy, and operational risk.

What risks concern global investors most heading into 2026?

Cyber risks lead at 55%, followed by technological disruption (53%), inflation (44%), macroeconomic volatility (43%), and geopolitical conflict (42%). Climate change (25%), ageing workforce (19%), and social inequality (16%) rank lower. Investors see these risks as interconnected, requiring comprehensive resilience strategies rather than siloed risk management approaches.

Why are investors favoring cross-sector business expansion over focused models?

PwC’s survey shows investors increasingly prefer companies that expand across traditional sector boundaries. As industries converge through technology platforms, cross-sector agility enables deeper competitive moats, diversified revenue streams, and greater value chain capture. However, this expansion must be technology-driven and strategic rather than opportunistic diversification.

How important is sustainability reporting to institutional investors in 2025?

While only 39-45% of investors heavily rely on sustainability disclosures for risk assessment, 78% believe providing sustainability information has a very or moderately positive impact on investor engagement. This indicates that ESG reporting is transitioning from optional to baseline expectation, with emphasis on connecting sustainability metrics directly to financial performance.